Understanding how much you can save with dental insurance becomes essential when planning your healthcare budget, especially as dental costs continue rising across Texas. Many patients wonder whether dental insurance premiums justify the expense or if paying out-of-pocket makes more financial sense. The answer depends on your oral health needs, the frequency of dental visits, and the type of coverage you select. With routine cleanings costing between $75 and $200 per visit and major procedures like crowns or root canals reaching thousands of dollars, having the right insurance plan can significantly reduce your financial burden while encouraging you to maintain optimal oral health through regular preventive care.

Understanding Dental Insurance Coverage Tiers

Dental insurance typically operates on a tiered coverage structure that determines how much you'll save on various procedures. This system categorizes treatments into three distinct levels, each with different reimbursement rates that directly impact your out-of-pocket expenses.

Preventive Care Coverage

Most dental insurance plans cover 100% of preventive services, which include routine exams, cleanings, and X-rays. These benefits typically require no deductible and represent the foundation of how much can save with dental insurance through early problem detection. Patients who leverage their preventive benefits twice annually avoid more costly treatments down the road.

Standard preventive services covered at 100% include:

- Biannual dental examinations

- Professional teeth cleanings

- Diagnostic X-rays (bitewing and panoramic)

- Fluoride treatments for children

- Sealant applications

The average cost of a routine cleaning without insurance ranges from $75 to $200, while comprehensive exams add another $50 to $150. With two visits per year, you're looking at potential savings of $250 to $700 annually just from preventive coverage alone.

Basic Restorative Procedures

Basic procedures typically receive 70-80% coverage after you meet your deductible. This tier includes common treatments that address minor to moderate dental issues requiring intervention beyond preventive maintenance.

| Procedure | Average Cost Without Insurance | With 80% Coverage | Your Savings |

|---|---|---|---|

| Dental Filling | $150-$450 | $30-$90 | $120-$360 |

| Simple Extraction | $75-$300 | $15-$60 | $60-$240 |

| Root Canal | $700-$1,500 | $140-$300 | $560-$1,200 |

Major Dental Work Coverage

Major procedures receive 50% coverage under most plans, representing treatments that involve significant restoration or replacement of teeth. While the co-insurance percentage is lower, the actual dollar savings can be substantial given the high cost of these treatments.

According to detailed analysis of dental insurance costs by state, major work represents where insurance delivers the most dramatic financial protection. A single dental crown costs between $800 and $3,000 without insurance, but with 50% coverage, you'd pay $400 to $1,500, saving an equivalent amount.

Calculating Real Savings Scenarios

Understanding how much can save with dental insurance requires examining realistic scenarios based on different patient profiles and dental needs. The calculations below assume a typical individual plan with a $50 annual deductible and $1,500 maximum annual benefit.

Scenario One: Healthy Patient with Minimal Needs

Consider a patient who maintains excellent oral health and requires only preventive care annually. Their typical utilization includes two cleanings, two exams, and one set of bitewing X-rays.

Annual costs without insurance:

- Two cleanings: $300

- Two exams: $200

- X-rays: $100

- Total: $600

Annual costs with insurance:

- Premium: $360 ($30/month)

- Out-of-pocket: $0 (preventive covered 100%)

- Total: $360

- Net savings: $240

Even with minimal dental needs, this patient saves $240 annually while ensuring they maintain consistent preventive care habits. When you factor in potential emergency situations or unexpected needs, having insurance coverage at a dental clinic provides additional security.

Scenario Two: Patient Requiring Basic Restorative Work

A more typical scenario involves a patient who needs preventive care plus several fillings or a minor procedure during the year.

Annual costs without insurance:

- Preventive care: $600

- Three fillings: $900

- One simple extraction: $200

- Total: $1,700

Annual costs with insurance:

- Premium: $360

- Deductible: $50

- Fillings (20% of $900): $180

- Extraction (20% of $200): $40

- Total: $630

- Net savings: $1,070

This scenario demonstrates how much can save with dental insurance when addressing common dental issues. The savings exceed the annual premium by more than three times, making insurance a financially sound investment.

Scenario Three: Patient Needing Major Dental Work

Patients requiring major procedures benefit most dramatically from insurance coverage. Consider someone needing a crown, root canal, and routine preventive care.

Annual costs without insurance:

- Preventive care: $600

- Root canal: $1,200

- Crown: $1,500

- Total: $3,300

Annual costs with insurance:

- Premium: $360

- Deductible: $50

- Root canal (50% of $1,200): $600

- Crown (50% of $1,000): $500 (remainder hits annual maximum)

- Total: $1,510

- Net savings: $1,790

The insurance maximum typically limits benefits to $1,000-$2,000 annually, but even with this cap, savings remain substantial. Understanding the value of comprehensive dental coverage becomes especially clear when facing expensive procedures.

Hidden Savings Beyond Direct Procedure Costs

The financial benefits of dental insurance extend beyond simple procedure discounts. Several indirect savings factors contribute to the total value proposition that many patients overlook when evaluating coverage options.

Negotiated Fee Schedules

Insurance companies negotiate contracted rates with in-network providers, meaning the starting price for procedures is often lower than what uninsured patients pay. These negotiated fees represent immediate savings before insurance benefits even apply.

Example of negotiated rates:

| Procedure | Retail Price | Negotiated Rate | Savings Before Benefits |

|---|---|---|---|

| Crown | $1,500 | $1,000 | $500 |

| Root Canal | $1,400 | $950 | $450 |

| Bridge | $3,500 | $2,400 | $1,100 |

This discount structure means that even if you've exhausted your annual maximum, you still benefit from reduced pricing through the insurance network. Patients at facilities like Dental Plus Clinic locations across Texas can take advantage of these negotiated rates.

Prevention Incentive and Long-Term Cost Avoidance

Insurance coverage encourages regular preventive visits by eliminating cost barriers. This behavioral nudge leads to earlier problem detection and intervention, preventing minor issues from escalating into expensive major treatments.

Research consistently shows that patients with insurance:

- Visit the dentist 40% more frequently than uninsured patients

- Require 30% fewer emergency dental procedures

- Experience lower rates of tooth loss and advanced periodontal disease

- Maintain better overall oral health metrics

The compounding savings from prevention can easily exceed $1,000-$2,000 over a five-year period when compared to patients who delay care until problems become severe.

Tax Advantages for Self-Employed Individuals

Self-employed individuals can deduct dental insurance premiums as a business expense, effectively reducing the net cost of coverage. This tax benefit adds another layer of savings that improves the overall value equation.

If you're in the 22% tax bracket and pay $500 annually for dental insurance, your after-tax cost is effectively $390. This $110 reduction in real premium cost enhances how much can save with dental insurance when you factor in both coverage benefits and tax efficiency.

Comparing Individual, Family, and Group Plans

The type of plan you select significantly impacts your potential savings. Understanding the cost structure and benefit differences between plan types helps you optimize your coverage decision.

Individual Plan Economics

Individual dental plans typically cost between $15 and $50 monthly, with average premiums around $360 annually according to analysis of dental insurance premiums. These plans work best for single adults with predictable dental needs.

Typical individual plan structure:

- Monthly premium: $30

- Annual deductible: $50

- Preventive coverage: 100%

- Basic coverage: 80%

- Major coverage: 50%

- Annual maximum: $1,500

Family Plan Advantages

Family plans offer substantial per-person savings when covering multiple household members. While monthly premiums range from $50 to $150, the per-person cost decreases significantly compared to purchasing individual plans.

Family plan cost breakdown:

| Family Size | Average Monthly Premium | Per Person Cost | Individual Plans Total | Monthly Savings |

|---|---|---|---|---|

| 2 People | $65 | $32.50 | $60 | -$5 |

| 3 People | $90 | $30 | $90 | $0 |

| 4 People | $120 | $30 | $120 | $0 |

| 5 People | $145 | $29 | $150 | $5 |

Family plans typically include embedded deductibles (individual and family maximums) and may waive deductibles for children's preventive care. These features enhance value when managing dental care for multiple family members across locations like Dental Plus Clinic in New Braunfels or other Texas cities.

Employer-Sponsored Group Coverage

Group dental insurance through employers represents the most cost-effective option, with employers typically covering 50-70% of premiums. Employees might pay $10-$25 monthly for individual coverage or $30-$75 for family plans.

The value proposition of group plans includes:

- Substantially lower premiums due to employer subsidies

- No medical underwriting or waiting periods for existing employees

- Higher annual maximums (often $2,000-$2,500)

- Better coverage percentages on major work

- Integrated benefits with vision and medical insurance

For employees with access to group coverage, how much can save with dental insurance becomes even more favorable, as the low premium cost means nearly any dental utilization generates positive returns.

Dental Insurance vs. Alternative Savings Options

While traditional insurance offers significant value, alternative approaches like dental savings plans deserve consideration based on your specific circumstances and budget constraints.

Dental Savings Plan Structure

Dental savings plans operate as membership programs rather than insurance, offering discounts of 10-60% on procedures through participating providers. Annual membership costs range from $80 to $200 for individuals.

Key differences between savings plans and insurance:

| Feature | Dental Insurance | Dental Savings Plan |

|---|---|---|

| Structure | Risk pooling with premiums | Membership discount program |

| Annual Cost | $360-$600 | $80-$200 |

| Waiting Periods | Yes (0-12 months) | No |

| Annual Maximums | Yes ($1,000-$2,000) | No |

| Pre-existing Conditions | May affect coverage | No restrictions |

| Claims/Paperwork | Required | Not required |

Understanding the differences between insurance and savings plans helps you choose the option that maximizes your savings based on anticipated dental needs.

When Savings Plans Make Financial Sense

Dental savings plans work best for patients who need extensive work exceeding insurance annual maximums or those who missed enrollment periods for traditional coverage. The comparison between dental savings plans and traditional insurance reveals specific scenarios where each option excels.

Savings plans provide advantages for:

- Patients requiring treatment costing more than $2,000 annually

- Individuals needing immediate major work without waiting periods

- Those who prefer predictable discount percentages

- People managing multiple expensive procedures across one year

A patient needing $5,000 in dental work might pay $200 for a savings plan membership and receive 30% discounts, paying $3,500 for treatment (total: $3,700). Traditional insurance would cover $1,500 maximum, leaving $3,500 plus the $360 premium (total: $3,860), making the savings plan slightly more economical in this specific scenario.

Hybrid Strategy for Maximum Savings

Some patients optimize savings by strategically using both options. They maintain traditional insurance for preventive and basic care while purchasing a savings plan membership to access discounts on major work exceeding their annual maximum.

This hybrid approach requires careful cost-benefit analysis but can deliver the best possible savings for patients with high dental needs. Facilities offering multiple payment options, like those at Dental Plus Clinic in Seguin with savings plans, provide flexibility to implement this strategy.

Geographic Variations in Savings Potential

Where you live significantly impacts how much can save with dental insurance due to regional differences in dental costs, insurance premiums, and provider availability across Texas.

Texas Regional Cost Differences

Dental procedure costs vary notably between urban and rural Texas markets. Major metropolitan areas like Austin, San Antonio, and Houston typically command higher fees than smaller cities, affecting both uninsured costs and insurance savings potential.

Average procedure costs by Texas region:

| Procedure | Urban Texas | Rural Texas | Difference |

|---|---|---|---|

| Cleaning | $120 | $85 | $35 |

| Filling | $200 | $165 | $35 |

| Crown | $1,200 | $950 | $250 |

| Root Canal | $1,100 | $875 | $225 |

These regional variations mean that insurance provides greater absolute dollar savings in high-cost areas, though the percentage savings remain relatively consistent. Patients visiting providers in cities like Leander or Converse may experience different cost structures.

Network Density and Access

Insurance value also depends on the availability of in-network providers in your area. Urban centers offer extensive provider networks, while rural areas may have limited options, potentially requiring out-of-network visits with reduced benefits.

Factors affecting network access:

- Provider concentration in metropolitan versus rural areas

- Specialist availability for procedures like orthodontics or oral surgery

- Travel costs to reach in-network providers

- Appointment availability and wait times

When evaluating insurance options, verify that quality providers exist within reasonable distance of your location. Resources for finding dentists accepting insurance in Texas help ensure you can fully utilize your benefits.

Maximizing Your Insurance Benefits

Strategic utilization of dental insurance significantly increases how much can save with dental insurance beyond basic coverage. Understanding timing, benefit coordination, and plan optimization helps you extract maximum value from your coverage.

Timing Major Procedures Strategically

The annual maximum benefit resets each calendar year, creating opportunities to split expensive treatments across two benefit periods and effectively double your coverage.

Example of strategic timing:

- December 2026: Crown preparation and temporary placement (uses $500 of 2026 maximum)

- January 2027: Permanent crown placement (uses $500 of 2027 maximum)

- Total procedure cost: $1,500

- Insurance covers: $1,000 (instead of $500 if completed in single year)

- Your savings: Additional $500

This approach works for treatments that can be reasonably divided, such as multiple crowns, bridges, or staged implant procedures. Coordinating with your dentist to optimize treatment timing across benefit years maximizes insurance value.

Using All Preventive Benefits

Many insured patients fail to schedule both allowed cleanings annually, leaving preventive benefits unused. Since insurance covers these visits at 100%, each missed appointment represents wasted value already paid for through premiums.

Preventive benefit utilization checklist:

- Schedule both annual cleanings (typically six months apart)

- Complete any recommended X-rays within coverage allowances

- Utilize fluoride treatments if covered

- Apply sealants for children when appropriate

- Attend comprehensive exams, not just cleaning appointments

Maximizing preventive benefits ensures you receive full value while maintaining oral health that prevents costly future treatments. Regular visits to facilities offering comprehensive dental exams and cleanings help you stay current with preventive care.

Coordinating Dual Coverage

Patients with access to two insurance plans (common with married couples both having employer coverage) can coordinate benefits to cover more of their dental expenses. The primary plan pays first, then the secondary plan covers some or all of the remaining balance.

Coordination of benefits example:

| Cost Element | Amount | Primary Plan | Secondary Plan | Your Cost |

|---|---|---|---|---|

| Crown | $1,200 | $600 (50%) | $300 (50% of remainder) | $300 |

| Without dual coverage | – | $600 (50%) | – | $600 |

| Additional savings | – | – | $300 | $300 |

While paying premiums for two plans may not always be cost-effective, situations where employers substantially subsidize coverage make dual coordination a valuable strategy. The combined coverage can reduce out-of-pocket expenses to 10-20% for major procedures.

Special Considerations for Specific Treatments

Certain dental procedures present unique insurance considerations that affect potential savings. Understanding coverage nuances for common treatments helps you accurately project costs and plan accordingly.

Orthodontic Treatment Coverage

Adult orthodontics receives limited or no coverage under many dental insurance plans, while children's orthodontic treatment typically includes separate lifetime maximums ranging from $1,000 to $2,000. This specialized benefit significantly impacts savings for families with orthodontic needs.

Orthodontic coverage typically includes:

- Separate lifetime maximum (not annual)

- Age restrictions (often coverage ends at 18-19 years)

- Percentage coverage of 50% up to the maximum

- Requirement for specific bite or alignment criteria

Traditional braces cost $3,000-$7,000, making a $1,500 insurance benefit a meaningful contribution. However, comprehensive orthodontic treatments often exceed insurance maximums, requiring patients to budget for remaining costs.

Cosmetic Dentistry Limitations

Insurance categorizes procedures based on medical necessity, generally excluding purely cosmetic treatments. This distinction affects coverage for procedures that enhance appearance without addressing health issues.

Typically not covered cosmetic procedures:

- Teeth whitening for aesthetic purposes

- Veneers for cosmetic improvement

- Gum contouring for appearance

- Smile makeovers without functional need

However, when cosmetic procedures address functional problems (broken teeth, severe wear, bite issues), insurance may provide partial coverage. Discussing treatment justification with your provider helps maximize potential benefits. Services like porcelain veneers or teeth whitening might qualify for coverage depending on circumstances.

Dental Implant Coverage Variability

Dental implant coverage varies dramatically between plans, with some classifying implants as cosmetic or experimental and others covering them as major restorative work. This inconsistency significantly impacts how much can save with dental insurance for tooth replacement.

Implant coverage scenarios:

| Plan Type | Coverage Level | Out-of-Pocket for $3,000 Implant |

|---|---|---|

| No Coverage | 0% | $3,000 |

| Partial Coverage | 50% up to maximum | $1,500-$2,000 |

| Standard Major | 50% | $1,500 |

Plans offering implant coverage treat them as major procedures with 50% co-insurance, potentially saving $1,500-$2,500 per implant. Given that full-mouth reconstruction with dental implants can exceed $20,000, confirming implant coverage before committing to treatment becomes essential. Advanced options like All-on-4 versus All-on-6 implants involve substantial costs where insurance coverage dramatically affects affordability.

Emergency Dental Care and Insurance Value

Unexpected dental emergencies represent situations where insurance value becomes immediately apparent, as urgent care often requires expensive immediate treatment without opportunity for price shopping or planning.

Common Dental Emergencies and Costs

Emergency dental situations range from knocked-out teeth to severe infections requiring immediate intervention. Without insurance, these urgent visits combine diagnostic costs, after-hours fees, and treatment expenses.

Emergency scenarios and typical costs:

- Severe toothache requiring emergency exam and treatment: $200-$500

- Knocked-out tooth requiring repositioning and stabilization: $300-$800

- Cracked tooth needing emergency crown: $1,000-$2,000

- Dental abscess requiring drainage and antibiotics: $300-$600

- Broken restoration needing immediate repair: $150-$400

Insurance coverage for dental emergencies typically follows standard benefit percentages, with diagnostic exams and X-rays covered as preventive or basic care and treatments following tier-appropriate coverage levels.

After-Hours and Weekend Care

Emergency dental care outside regular business hours often includes facility fees or premium charges that insurance may or may not fully cover. Understanding your plan's emergency provisions helps you anticipate costs during urgent situations.

Most insurance plans cover emergency examinations and necessary treatment at standard rates regardless of timing, though some providers charge additional fees for after-hours access. Confirming emergency coverage details when selecting insurance ensures you understand potential out-of-pocket costs during crisis situations.

The Peace of Mind Factor

Beyond measurable financial savings, dental insurance provides psychological benefits by removing cost as a barrier to seeking timely care. Patients with coverage address problems earlier rather than delaying treatment due to expense concerns.

This behavioral difference translates to better health outcomes and lower long-term costs. Studies indicate insured patients seek emergency care 48 hours sooner on average than uninsured patients, reducing complication rates and improving treatment success.

Evaluating Your Personal Savings Potential

Determining how much can save with dental insurance requires honest assessment of your oral health history, risk factors, and anticipated needs. This personalized evaluation reveals whether insurance represents a sound financial investment for your specific situation.

Dental Health Risk Assessment

Your likelihood of needing dental work correlates strongly with several identifiable risk factors that should influence your insurance decision.

High-risk indicators suggesting insurance value:

- History of cavities or gum disease

- Previous root canals, crowns, or major work

- Poor oral hygiene habits

- Dietary habits promoting tooth decay (frequent sugar, acid exposure)

- Grinding or clenching teeth (bruxism)

- Tobacco use

- Chronic health conditions affecting oral health (diabetes, autoimmune disorders)

- Family history of dental problems

Patients with multiple risk factors almost universally benefit from insurance coverage, as their probability of needing more than preventive care approaches 70-80% annually. The question shifts from whether insurance saves money to how much savings it will generate.

Creating a Personal Cost Projection

Building a realistic projection of dental expenses helps quantify insurance value for your circumstances. This exercise requires reviewing past dental work and estimating future needs.

Steps for personal cost projection:

- Review dental history from past 3-5 years

- Identify recurring issues or treatment patterns

- Account for age-related factors (increased needs over 40)

- Factor in known upcoming work (orthodontics, implants, etc.)

- Calculate average annual dental spending

- Compare against insurance premium and projected out-of-pocket costs

If your projected dental expenses consistently exceed $800-$1,000 annually, insurance typically delivers positive returns. Below this threshold, the value proposition becomes less clear and depends on risk tolerance and preventive care priorities.

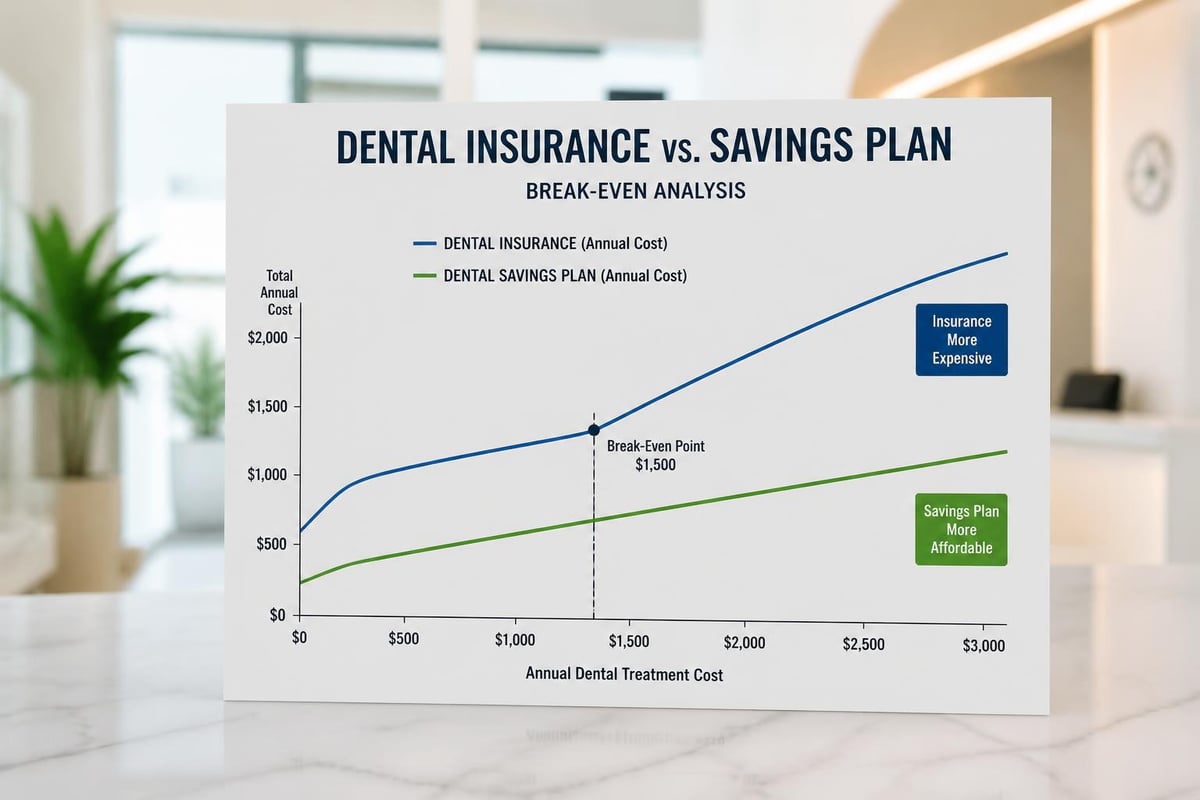

Break-Even Analysis

A simple break-even calculation reveals the annual dental expenses required to justify insurance premiums. This threshold helps you decide whether coverage makes financial sense.

Break-even calculation example:

- Annual premium: $360

- Average deductible: $50

- Break-even point: Dental work costing $600+ in a year

At the break-even point, insurance costs equal cash-pay costs, meaning any additional dental needs generate savings. Most adults require at least $600 in dental care annually when including preventive visits and occasional basic work, pushing most patients past break-even into positive savings territory.

Resources analyzing when dental insurance saves money versus cash payment provide additional context for this decision framework.

Hidden Costs That Reduce Insurance Value

While insurance provides substantial savings for many patients, certain factors can diminish its value. Understanding these limitations ensures realistic expectations and helps you avoid situations where insurance delivers less benefit than anticipated.

Annual Maximum Limitations

The annual benefit maximum represents the most significant constraint on insurance value for patients with extensive dental needs. Once you reach this limit (typically $1,000-$2,000), you pay 100% of additional costs despite continuing to pay premiums.

Maximum limitation impact example:

A patient needing two crowns ($3,000 total) with a $1,500 annual maximum receives:

- Insurance pays: $1,500 (50% coverage until maximum reached)

- Patient pays: $2,250 (50% of $1,500 covered plus 100% of remaining $1,500)

- Total patient cost: $2,250 plus $360 premium = $2,610

Without insurance:

- Patient pays: $3,000

- Net insurance savings: $390 (less than premium alone)

This scenario demonstrates how extensive needs can reduce insurance value, making alternative options like savings plans more attractive for high-cost situations. Comparing dental insurance with savings plans helps identify the best option for your circumstances.

Waiting Periods for Major Work

Most dental insurance plans impose waiting periods of 6-12 months for major procedures, meaning you pay premiums without access to full benefits during this time. This limitation particularly affects new enrollees with immediate needs.

Typical waiting period structure:

- Preventive care: No waiting period

- Basic procedures: 6-month waiting period

- Major procedures: 12-month waiting period

These waiting periods prevent immediate high utilization and protect insurance companies from adverse selection, but they reduce value for patients purchasing coverage specifically to address known problems. Planning dental work timing around waiting periods helps maximize benefit utilization.

Missing Tooth Clause

Many insurance plans include "missing tooth clauses" that exclude coverage for replacing teeth lost before coverage began. This provision prevents patients from purchasing insurance specifically to replace existing missing teeth.

The missing tooth clause significantly impacts savings potential for patients considering implants, bridges, or dentures for pre-existing tooth loss. While recent years have seen some insurers relax or eliminate these clauses, confirming coverage for tooth replacement remains essential during plan selection.

Pre-Authorization Requirements

Some procedures require pre-authorization before insurance commits to coverage, adding administrative complexity and potential for benefit denial. The pre-authorization process can delay treatment and create uncertainty about final costs.

Procedures commonly requiring pre-authorization:

- Dental crowns exceeding certain thresholds

- Periodontal treatments

- Dental implants

- Orthodontic work

- Full or partial dentures

While pre-authorization protects patients by confirming coverage before treatment, it can reveal limitations or exclusions that reduce anticipated savings. Working with experienced providers familiar with insurance requirements streamlines this process.

Understanding how much you can save with dental insurance depends on your individual oral health needs, coverage tier, and how effectively you utilize available benefits. For most patients, insurance delivers substantial savings through preventive care coverage, negotiated rates, and protection against expensive unexpected treatments. Whether you need routine maintenance, restorative work, or advanced procedures across our convenient locations in Texas, Dental Plus Clinic accepts most major insurance plans and works with you to maximize your benefits while delivering high-quality, compassionate dental care for your entire family.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}