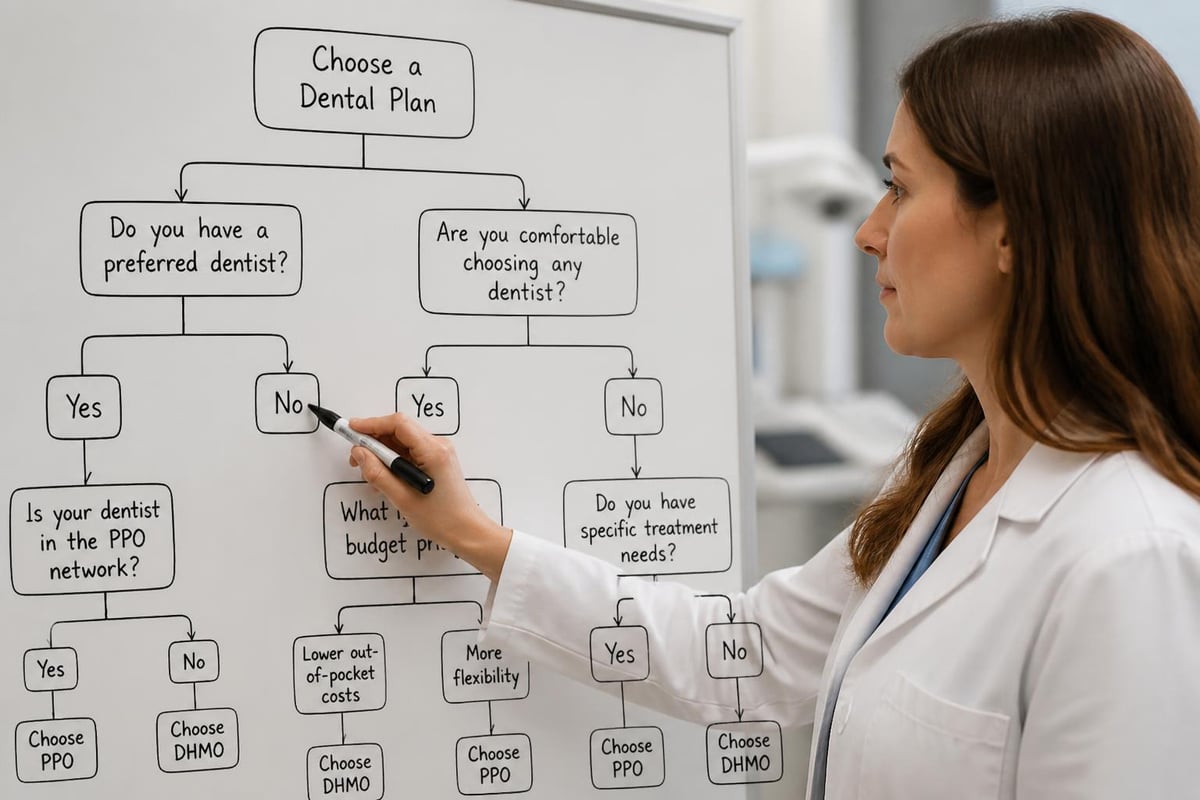

Choosing the right dental insurance can significantly impact your oral health and budget. When comparing ppo vs dhmo dental plans, many Texas residents struggle to understand which option provides better value for their specific needs. Each plan type offers distinct advantages and limitations that affect everything from monthly premiums to provider selection and out-of-pocket costs. Understanding these differences empowers you to make informed decisions about your family's dental coverage, ensuring access to quality care while managing expenses effectively.

Understanding PPO Dental Plans

Preferred Provider Organization (PPO) dental plans represent one of the most popular insurance options available across Texas. These plans create networks of dentists who agree to provide services at pre-negotiated rates, though they allow members considerable flexibility in choosing providers.

Network Flexibility and Out-of-Network Coverage

PPO plans distinguish themselves through their provider flexibility. You can visit any licensed dentist, whether they participate in your plan's network or not. In-network dentists offer the greatest savings because they've agreed to discounted fee schedules. When you visit out-of-network providers, your plan still provides coverage, though at reduced reimbursement rates.

This flexibility proves particularly valuable for patients who:

- Have established relationships with specific dentists

- Require specialized treatments not available within the network

- Travel frequently and need care in different locations

- Want freedom to choose providers based on convenience or reputation

The fundamental difference between PPO and HMO dental plans centers on this network flexibility, making PPOs attractive for those who prioritize choice.

Cost Structure and Financial Considerations

PPO dental plans typically feature higher monthly premiums compared to DHMO options. However, they often include deductibles and coinsurance requirements that affect your total costs.

| Cost Component | PPO Structure | Typical Range |

|---|---|---|

| Monthly Premium | Moderate to High | $30-$80 per person |

| Annual Deductible | Yes (usually waived for preventive) | $50-$150 |

| Preventive Coverage | 100% in-network | Cleanings, exams, X-rays |

| Basic Procedures | 70-80% after deductible | Fillings, extractions |

| Major Procedures | 50% after deductible | Crowns, bridges, implants |

Most PPO plans operate on a calendar-year maximum, typically ranging from $1,000 to $2,000 per person. Understanding these dental insurance structures helps you budget effectively for both routine and unexpected dental needs.

Understanding DHMO Dental Plans

Dental Health Maintenance Organization (DHMO) plans, also called capitated plans, operate fundamentally differently from PPOs. These plans emphasize affordability and preventive care through a more structured network approach.

Primary Care Dentist Selection

DHMO plans require you to select a primary care dentist from an approved network at enrollment. This dentist becomes your central point of contact for all dental services. If you need specialized care, your primary dentist provides referrals to network specialists.

This system creates several implications:

Benefits of the primary dentist model:

- Coordinated care with comprehensive treatment planning

- Established patient-provider relationship

- Simplified billing with predictable costs

- Focus on preventive care and early intervention

Limitations to consider:

- No coverage for out-of-network providers (except emergencies)

- Must change primary dentist if you move or they leave the network

- Limited specialist access without referrals

- Smaller provider networks in some areas

DHMO Pricing and Coverage

DHMO plans excel in affordability. Monthly premiums typically cost significantly less than PPO options, and most DHMOs eliminate deductibles entirely. According to Humana’s comparison of dental HMO vs PPO plans, DHMO members often pay fixed copayments for services rather than percentage-based coinsurance.

The copayment structure provides excellent cost predictability. You know exactly what each procedure costs before treatment begins. Many DHMO plans offer preventive services like cleanings and exams at no cost beyond the monthly premium.

Key Differences in PPO vs DHMO Dental Plans

When evaluating ppo vs dhmo dental plans, several critical factors distinguish these coverage types. Understanding these differences helps align your insurance choice with your healthcare preferences and financial situation.

Provider Network Restrictions

Network structure represents the most significant difference between these plans. PPO networks operate on a preferred-provider basis, meaning you receive maximum benefits from network dentists but retain coverage for out-of-network care. DHMO networks function on an exclusive basis-you must use network providers (except in emergencies) to receive any coverage.

For Texas families considering dental care options, this distinction matters considerably. Urban areas like Austin, San Antonio, and the surrounding communities typically offer robust DHMO networks, while rural regions may have limited participating providers.

Cost Comparison Analysis

The financial structures of ppo vs dhmo dental plans differ substantially:

| Feature | PPO Plans | DHMO Plans |

|---|---|---|

| Monthly Premium | $35-$80 individual | $15-$40 individual |

| Annual Deductible | $50-$150 | Usually $0 |

| Preventive Care | 100% coverage | Usually $0 copay |

| Basic Fillings | 20-30% coinsurance | $40-$80 copay |

| Root Canal | 50% coinsurance | $200-$350 copay |

| Crown | 50% coinsurance | $400-$600 copay |

| Annual Maximum | $1,000-$2,000 | Often unlimited |

DHMO plans eliminate the uncertainty of percentage-based coinsurance. You pay a predetermined copayment regardless of the dentist's usual fees. This predictability helps with budgeting, especially for families requiring multiple procedures throughout the year.

PPO plans may ultimately cost less for individuals who rarely need dental work beyond preventive care, despite higher premiums. The percentage-based coverage becomes valuable for major procedures that approach or exceed annual maximums.

Referral Requirements and Specialist Access

DHMO plans require referrals from your primary dentist before seeing specialists like orthodontists, periodontists, or oral surgeons. Your primary dentist coordinates these referrals and ensures continuity of care. This system works well when you trust your primary dentist's judgment and prefer coordinated treatment.

PPO plans eliminate referral requirements entirely. You can schedule appointments directly with any specialist, whether in-network or out-of-network. This direct access proves beneficial when you:

- Need immediate specialist consultation

- Prefer specialists based on reputation or location

- Require multiple specialist opinions

- Have complex dental conditions requiring coordinated specialty care

For patients considering advanced treatments like dental implants, direct specialist access may influence plan selection significantly.

Coverage for Common Dental Procedures

Understanding how ppo vs dhmo dental plans cover specific treatments helps you anticipate costs and make informed decisions about your oral health care.

Preventive Care Coverage

Both plan types emphasize preventive dentistry, though their approaches differ. PPO plans typically cover preventive services at 100% when using in-network providers, often without applying deductibles. These services include:

- Routine dental exams (usually twice yearly)

- Professional cleanings and fluoride treatments

- Diagnostic X-rays

- Oral cancer screenings

- Sealants for children

DHMO plans similarly prioritize prevention, frequently offering these services with zero copayment. This alignment reflects industry-wide recognition that preventive care reduces long-term costs by identifying problems early.

The comprehensive preventive care offered at practices accepting both plan types ensures regular maintenance regardless of your insurance choice.

Restorative Treatment Coverage

Restorative procedures like fillings, crowns, and bridges receive different coverage depending on plan type. PPO plans classify these as "basic" or "major" services, applying coinsurance after deductibles. A filling might cost you 20% of the negotiated fee, while a crown might require 50% coinsurance.

DHMO plans establish fixed copayments for each procedure. The comparison between DPPO and DHMO plans reveals that copayment amounts vary by network but remain consistent within each plan.

Orthodontic and Cosmetic Services

Orthodontic coverage varies significantly between plans and individual policies. Some PPO plans include orthodontic benefits with separate lifetime maximums (commonly $1,000-$1,500). DHMO plans may offer orthodontic coverage through network providers at substantial discounts, though coverage specifics depend on the particular plan.

Most dental insurance plans, whether PPO or DHMO, exclude purely cosmetic procedures like teeth whitening or porcelain veneers unless deemed medically necessary. However, practices often provide cash-pay discounts or payment plans for these services.

Choosing Between PPO and DHMO Plans

Selecting the optimal plan from ppo vs dhmo dental plans requires evaluating your personal circumstances, dental health status, and financial priorities. Neither option universally outperforms the other-the best choice depends on individual factors.

Assessing Your Dental Health Needs

Begin by evaluating your current oral health and anticipated treatment needs. Consider these questions:

Current dental status:

- Do you require ongoing treatment for existing conditions?

- Have you been diagnosed with periodontal disease or other chronic issues?

- Are you planning major dental work like implants or orthodontics?

- How frequently do you need dental care beyond routine cleanings?

Family considerations:

- Do children need orthodontic evaluation or treatment?

- Does anyone have special dental needs requiring specialist care?

- Are family members established with preferred dentists?

Individuals with excellent oral health who primarily need preventive care often find DHMO plans provide excellent value. Those requiring extensive treatment or specialist care may benefit from PPO flexibility despite higher costs.

Evaluating Provider Networks

Research available networks thoroughly before selecting between ppo vs dhmo dental plans. The strongest plan financially means little if quality providers aren't accessible.

Network evaluation steps:

- Review provider directories online

- Verify your current dentist's participation status

- Check proximity of network dentists to home and work

- Read patient reviews for network providers

- Confirm specialist availability within the network

Texas residents have access to various network sizes. Metropolitan areas surrounding Dental Plus Clinic locations in cities like Leander and New Braunfels typically offer robust networks for both plan types.

Financial Planning and Budget Analysis

Calculate total annual costs under realistic usage scenarios. Don't focus exclusively on monthly premiums-factor in all potential expenses.

PPO annual cost calculation:

- Monthly premium × 12

- Annual deductible

- Expected coinsurance for planned procedures

- Potential out-of-network costs

DHMO annual cost calculation:

- Monthly premium × 12

- Copayments for anticipated procedures

- Zero out-of-network coverage consideration

Create scenarios ranging from minimal use (preventive only) to moderate use (preventive plus several basic procedures) to heavy use (major restorative work). This analysis reveals which plan type offers better value for your expected utilization.

Common Misconceptions About Dental Plan Types

Several persistent myths about ppo vs dhmo dental plans lead to confusion and suboptimal insurance choices. Clarifying these misconceptions helps you make decisions based on facts rather than misunderstandings.

Quality of Care Myths

Misconception: DHMO plans provide inferior dental care compared to PPO plans.

Reality: Plan type doesn't determine care quality. Dentist qualifications, experience, and commitment to patient outcomes matter far more than insurance structure. Both PPO and DHMO networks include highly qualified, board-certified dentists who provide excellent care.

Network dentists must meet credentialing requirements regardless of plan type. Many dental practices accept both PPO and DHMO plans, providing identical care quality to all patients. The differences between PPO and DHMO structures relate to payment methodology and network rules, not clinical standards.

Coverage Limitation Misunderstandings

Misconception: PPO plans always cover more procedures than DHMO plans.

Reality: Both plan types typically cover the same categories of dental services-preventive, basic, and major procedures. The difference lies in how they pay for services, not which services qualify for coverage.

Some DHMO plans actually provide better coverage for certain procedures because they lack annual maximums. PPO maximums can create coverage gaps for patients requiring extensive treatment. According to information from Carnegie Mellon’s dental plan overview, both plan types serve different member needs effectively.

Network Size Assumptions

Misconception: PPO networks are always larger than DHMO networks.

Reality: Network size varies by insurance carrier and geographic region, not plan type. Some DHMO networks include hundreds of providers in specific areas, while certain PPO networks may have limited participation.

The practical network size that matters is local availability. A national network with 50,000 dentists provides little value if none practice within reasonable distance. Residents near Dental Plus Clinic’s Seguin location should evaluate network density specifically in their community.

Flexibility and Life Changes

Life circumstances change, affecting your dental insurance needs. Understanding how ppo vs dhmo dental plans accommodate change helps you select coverage that remains appropriate as your situation evolves.

Changing Dentists and Provider Relationships

PPO plans offer superior flexibility when changing dentists. You can switch providers anytime without notification or penalty. This freedom benefits patients who:

- Move to different cities or neighborhoods

- Experience dissatisfaction with current providers

- Seek second opinions or alternative treatment approaches

- Require immediate care when traveling

DHMO plans require formal primary dentist changes through your insurance carrier. While not particularly difficult, this process takes time and typically only allows changes during specific periods or for qualifying events. However, this structure encourages stable provider relationships that support continuity of care.

Geographic Mobility Considerations

Families anticipating relocation should weigh geographic flexibility heavily when comparing ppo vs dhmo dental plans. PPO plans maintain value across relocations because you can access new providers immediately. DHMO plans require verifying network adequacy in your destination before moving.

Texas residents moving between cities like Converse and Beeville should confirm that their DHMO network includes quality providers in both locations. The pros and cons of each plan type shift based on network availability in your specific area.

Family Growth and Changing Needs

Adding family members affects dental insurance considerations significantly. Evaluate how each plan type accommodates:

- Pregnancy and newborns: Some plans offer enhanced preventive care during pregnancy

- Children's dental development: Pediatric networks and orthodontic coverage availability

- Aging parents: Increased need for restorative and replacement procedures

- Special needs: Access to specialists and coordinated care requirements

Family coverage under DHMO plans typically costs substantially less than PPO alternatives, making them attractive for larger families focused on budget management.

Making the Switch Between Plan Types

Understanding when and how to transition between ppo vs dhmo dental plans helps you optimize coverage as circumstances change. Most people can modify coverage during annual open enrollment periods or following qualifying life events.

Timing Your Plan Change

Open enrollment represents the primary opportunity to switch dental plans. This period typically occurs once annually, though exact timing depends on your coverage source:

- Employer-sponsored plans: Usually coincide with health insurance enrollment

- Marketplace plans: Generally November through mid-January

- Individual plans: May offer monthly enrollment depending on carrier

Qualifying life events trigger special enrollment periods allowing mid-year changes. These events include marriage, divorce, birth or adoption, loss of coverage, or permanent relocation.

Coordinating Treatment Across Plan Changes

If you're undergoing multi-visit treatment when switching between plan types, careful coordination prevents coverage gaps and unexpected costs. Take these steps:

- Complete in-progress treatment before the plan change if possible

- Obtain pre-authorization from your new plan for continuing treatment

- Verify the new plan covers remaining procedures

- Confirm your dentist accepts the new insurance type

- Request detailed treatment records to share with new providers if changing dentists

The differences between insurance and savings plans also merit consideration during transitions, as dental savings plans offer alternatives to traditional insurance structures.

Maximizing Benefits During Transitions

Strategic timing optimizes dental benefits when switching plans:

Before year-end with current plan:

- Schedule remaining preventive visits

- Complete approved treatments

- Use remaining annual maximum benefits

- Submit pending claims

After new plan activation:

- Schedule preventive care to establish benefit usage

- Obtain treatment plans and pre-authorizations for planned work

- Verify coverage details directly with the carrier

- Update provider office with new insurance information

Regional Considerations for Texas Residents

Geographic factors influence how ppo vs dhmo dental plans perform for Texas residents. Understanding regional dynamics helps you select coverage aligned with local healthcare infrastructure and costs.

Provider Density Across Texas Regions

Urban areas like Austin, San Antonio, and Houston feature dense dental provider networks for both PPO and DHMO plans. Suburban and rural regions may have limited DHMO participation, making PPO plans more practical despite higher costs.

Central Texas communities benefit from strong dental provider presence. Cities hosting Dental Plus Clinic locations offer patients multiple network options under both plan types, supporting informed choice based on financial and preference factors rather than availability constraints.

Cost of Living and Premium Variations

Dental insurance premiums reflect regional cost-of-living differences. Metropolitan areas typically feature higher premiums for both plan types, though the gap between ppo vs dhmo dental plans remains consistent proportionally.

| Texas Region | Average PPO Premium | Average DHMO Premium | Provider Density |

|---|---|---|---|

| Urban Core | $45-$75/month | $20-$35/month | High |

| Suburban | $40-$65/month | $18-$30/month | Moderate-High |

| Rural | $35-$55/month | $15-$25/month | Low-Moderate |

These figures represent individual coverage estimates for 2026 and vary by specific carrier and plan design.

State-Specific Insurance Regulations

Texas maintains specific insurance regulations affecting dental coverage availability and consumer protections. The Texas Department of Insurance oversees plan offerings, ensuring carriers meet minimum standards and maintain adequate networks.

State regulations require insurance companies to provide clear disclosure of coverage limitations, network directories, and appeals processes. These protections apply equally to PPO and DHMO plans, safeguarding consumers regardless of plan type selection.

Employer-Sponsored vs Individual Plans

The source of your dental insurance-employer-sponsored or individually purchased-affects how you evaluate ppo vs dhmo dental plans. Each scenario presents unique considerations and decision factors.

Employer Plan Selection Strategies

Many employers offer both PPO and DHMO options during open enrollment. Employer contributions typically favor the less expensive option (usually DHMO), making it more attractive financially. However, evaluate total value rather than just premium differences.

Questions to ask your HR department:

- What percentage of the premium does the employer cover for each plan?

- Are network directories available for review?

- Can you speak with current plan members about their experiences?

- What is the process for changing plans in future years?

- Are dental savings accounts or FSAs available to supplement coverage?

Employer plans often negotiate better rates than individual coverage, making even PPO options more affordable than comparable individual market plans.

Individual Market Considerations

Purchasing dental insurance independently provides complete control over plan selection but eliminates employer premium contributions. This scenario makes cost differences between ppo vs dhmo dental plans more significant to your budget.

Individual plans often feature:

- Higher premiums than employer-sponsored equivalents

- More restrictive networks in some areas

- Greater variation in coverage specifics between carriers

- Simplified underwriting with limited or no health questions

The DHMO vs PPO insurance differences become more pronounced in individual markets where you bear full premium costs.

Alternative and Supplemental Options

Beyond traditional ppo vs dhmo dental plans, alternative coverage approaches merit consideration. These options sometimes provide better value or complement existing insurance.

Dental Savings Plans

Dental savings plans function differently from insurance, offering discounted fee schedules rather than claims-based coverage. Members pay annual fees (typically $80-$200) and receive 10-50% discounts on dental services from participating providers.

These plans work well for:

- Individuals without employer-sponsored coverage

- Those requiring extensive dental work exceeding insurance maximums

- Patients whose preferred dentists don't accept insurance

- Families seeking predictable, affordable dental care

Some practices, including those offering dental savings programs, provide in-house discount plans as alternatives to traditional insurance.

Supplemental Coverage Strategies

Combining coverage approaches optimizes benefits for complex dental needs. Consider these strategies:

- Primary insurance plus discount plan: Use insurance for covered services and discount plan for exclusions

- Dual coverage through spouses: Coordinate benefits when both partners have employer coverage

- FSA or HSA supplementation: Use tax-advantaged accounts for out-of-pocket costs

- Catastrophic plus routine: Maintain minimal insurance for major procedures while paying cash for preventive care

The comparison of HMO and PPO plans provides additional context for evaluating how these options complement or substitute for traditional insurance.

Questions to Ask Before Enrolling

Before finalizing your decision between ppo vs dhmo dental plans, obtain clear answers to critical questions. These inquiries prevent surprises and ensure your chosen plan meets expectations.

Coverage and Benefit Questions

Essential questions for any dental plan:

- What specific procedures are covered under preventive, basic, and major categories?

- Are there waiting periods before coverage begins for certain procedures?

- What is the annual maximum benefit, if any?

- How does the plan handle pre-existing conditions?

- Are implants, orthodontics, or cosmetic procedures covered?

- What happens if I need emergency care outside the network or service area?

Network and Provider Questions

Critical network inquiries:

- How many dentists participate in my local area?

- Is my current dentist in-network?

- Can I see specialists without referrals?

- What happens if my dentist leaves the network mid-year?

- Are there adequate pediatric dentists if I have children?

Administrative and Claims Questions

Understanding administrative processes prevents frustration:

- How do I submit claims for reimbursement (PPO out-of-network)?

- What is the typical claims processing timeframe?

- Can I access plan information and benefits online?

- What is the appeals process if a claim is denied?

- Are there exclusions or limitations I should know about?

These questions apply to both PPO and DHMO structures, though specific answers vary by plan type. The DHMO versus PPO comparison highlights how administrative experiences differ between plan types.

Long-Term Value Assessment

Evaluating ppo vs dhmo dental plans requires looking beyond immediate costs to long-term value and oral health outcomes. The cheapest plan today may not provide optimal value over time.

Total Cost of Ownership Analysis

Calculate five-year total costs under different scenarios:

Conservative scenario (minimal dental needs):

- Annual preventive visits only

- Occasional minor procedures

- No major restorative work

Moderate scenario (average dental needs):

- Regular preventive care

- Several fillings or minor procedures annually

- One crown or major procedure over five years

Intensive scenario (significant dental needs):

- Preventive care plus ongoing treatment

- Multiple major procedures

- Potential specialist care

Running these calculations for both plan types reveals which offers better long-term value based on your realistic dental health trajectory.

Health Outcome Considerations

The best dental plan supports optimal oral health, not just minimal spending. Consider how plan structure affects:

- Preventive care utilization: Do low/no costs for cleanings encourage regular visits?

- Treatment acceptance: Will out-of-pocket costs cause you to delay necessary care?

- Provider relationship: Does the plan support continuity with trusted dentists?

- Comprehensive treatment: Can you afford recommended care under the plan structure?

Delaying necessary treatment due to cost concerns often leads to more extensive, expensive procedures later. A plan encouraging timely treatment may provide better long-term value despite higher premiums.

Quality of Life Factors

Dental insurance affects quality of life beyond clinical outcomes. Consider intangible factors:

- Stress reduction: How much mental energy does managing dental benefits require?

- Convenience: Does the plan work with your schedule and location preferences?

- Family satisfaction: Are all household members comfortable with covered providers?

- Financial predictability: Can you budget confidently with the cost structure?

These factors, while difficult to quantify, significantly impact your satisfaction with chosen coverage.

Selecting between PPO and DHMO dental plans requires careful evaluation of your unique circumstances, priorities, and oral health needs. Neither option universally outperforms the other, making informed choice essential for maximizing value and maintaining excellent dental health. At Dental Plus Clinic, we accept multiple insurance plans and work with patients across our Texas locations to optimize their coverage benefits while delivering comprehensive, high-quality dental care. Our team helps you understand your insurance options and creates treatment plans that align with your coverage, ensuring accessible, affordable dental health for you and your family.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}