Understanding the difference between in-network vs out-of-network dentists can significantly impact your family's dental care costs and access to quality treatment. With dental insurance plans becoming increasingly complex, Texas patients need clarity about how network status affects their out-of-pocket expenses, coverage levels, and overall dental experience. Making an informed decision about whether to stay within your insurance network or venture outside can save you hundreds or even thousands of dollars annually while ensuring you receive the comprehensive care your family deserves.

Understanding Dental Insurance Networks

Dental insurance networks consist of providers who have negotiated contracts with insurance companies to deliver services at pre-determined rates. These contractual agreements create a framework that defines which dentists are considered in-network and which operate outside the network boundaries.

Insurance companies build networks by recruiting dental practices willing to accept discounted fee schedules in exchange for patient referrals. The differences between in-network and out-of-network dental providers extend beyond simple pricing structures to include claim processing procedures, coverage percentages, and administrative responsibilities.

How Network Agreements Work

Network agreements establish specific reimbursement rates for every procedure code. Dentists who join these networks agree to:

- Accept predetermined fees for covered services

- Submit claims directly to insurance carriers

- Adhere to network-specific administrative requirements

- Provide documentation according to carrier standards

- Follow appeals processes for disputed claims

Out-of-network providers maintain full autonomy over their fee schedules but sacrifice guaranteed patient flow from insurance referrals. This independence allows them to set prices based on their operational costs, expertise, and market positioning rather than accepting insurance-dictated rates.

The relationship between insurance carriers and dental practices shapes the entire reimbursement ecosystem. Understanding these dynamics helps patients make strategic decisions about where to receive care and how to maximize their benefits.

Financial Implications of Network Status

Cost differences between network options represent the most tangible factor influencing patient decisions. The financial gap between in-network and out-of-network care varies dramatically based on your specific plan design and the procedures you need.

In-network providers typically offer lower out-of-pocket costs because insurance companies reimburse a higher percentage of the negotiated fee. Most dental plans cover 80-100% of preventive services, 70-80% of basic procedures, and 50% of major treatments when you visit network dentists.

Out-of-Network Cost Structures

When you choose an out-of-network dentist, your insurance company typically:

- Calculates benefits based on their "usual and customary" (UCR) rates

- Pays a lower percentage of the total fee

- Subjects you to balance billing for amounts exceeding UCR

- Applies higher deductibles in some plan designs

- Counts expenses differently toward annual maximums

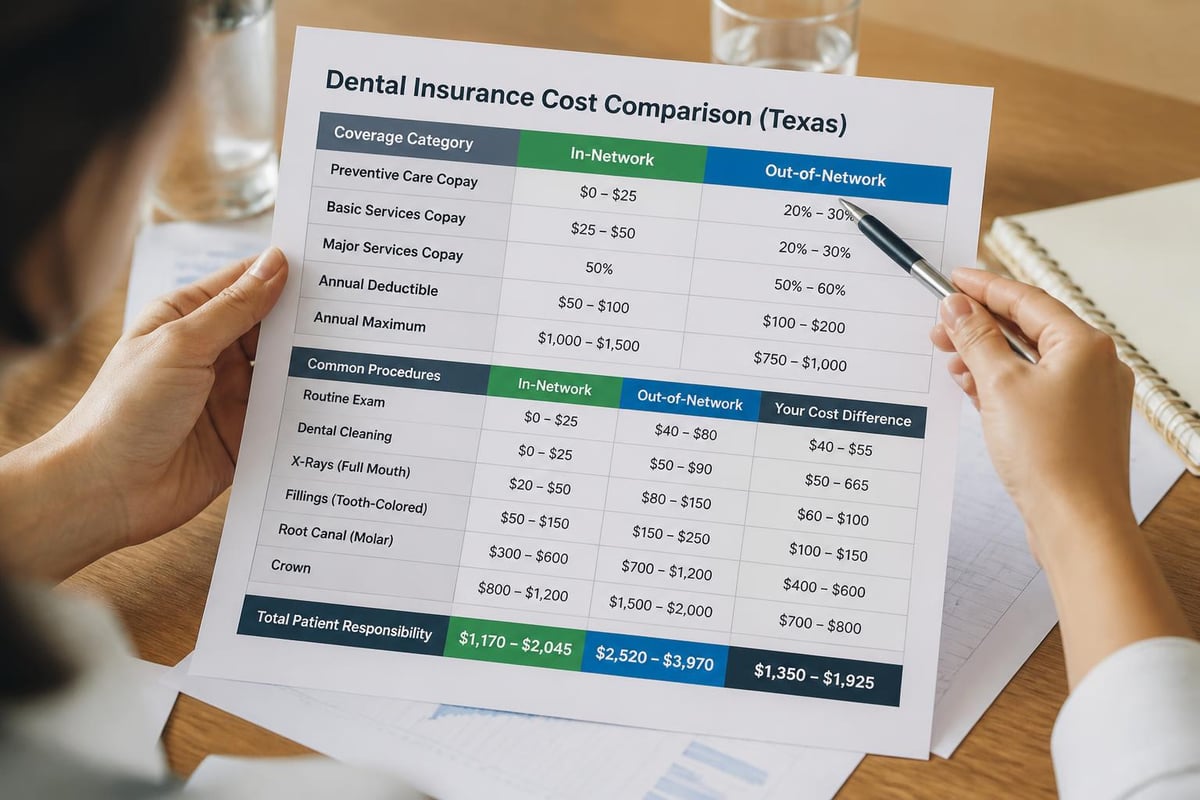

| Cost Factor | In-Network | Out-of-Network |

|---|---|---|

| Preventive Coverage | 80-100% | 50-80% |

| Basic Procedures | 70-80% | 50-70% |

| Major Services | 50% | 30-50% |

| Balance Billing | Not Allowed | Often Applied |

| Annual Deductible | $25-50 | $50-100 |

These percentage differences translate to real dollars. A routine cleaning might cost you nothing in-network but $50-75 out-of-network. A crown could mean paying $500 versus $800-1,000 depending on network status.

Balance billing represents a critical financial consideration when evaluating out-of-network dentists. This practice allows dentists to bill patients for the difference between their actual charges and what insurance deems reasonable, potentially creating unexpected expenses.

Coverage Levels and Reimbursement Rates

Insurance reimbursement varies substantially based on network participation. The financial implications of choosing out-of-network dental services extend beyond simple copayment differences to affect how insurance companies process and pay claims.

In-network dentists accept the insurance company's fee schedule as payment in full (minus patient cost-sharing). This arrangement provides cost predictability because you know exactly what you'll pay before treatment begins.

Maximum Annual Benefits

Most dental plans impose annual maximum benefit limits, typically ranging from $1,000 to $2,500 per person. Network status affects how quickly you reach these limits:

- In-network visits: Insurance pays larger portions, preserving more of your annual maximum

- Out-of-network visits: Lower reimbursement percentages exhaust benefits faster

- Combined maximums: Some plans share limits regardless of network status

- Separate maximums: Certain plans offer distinct limits for network and non-network care

For families requiring extensive dental work, staying in-network can stretch annual benefits significantly further. A family of four needing routine preventive care plus several fillings might use only 60-70% of their annual maximum in-network versus exhausting the entire benefit out-of-network.

Understanding how your specific plan calculates benefits requires reviewing your dental insurance terms and coverage details. Plan documents outline exact reimbursement percentages, fee schedules, and maximum benefit structures.

Quality of Care Considerations

Financial factors dominate most discussions about in-network vs out-of-network dentists, but care quality deserves equal attention. Network status doesn't inherently indicate provider competence, experience, or treatment philosophy.

Exceptional dentists practice both within and outside insurance networks. The decision to join networks often reflects business strategy rather than clinical capability. Some highly qualified dentists deliberately remain out-of-network to maintain clinical autonomy and avoid insurance-imposed treatment limitations.

Evaluating Dentist Credentials

Regardless of network status, assess potential dentists based on:

- Education and training: Dental school attended, continuing education participation

- Board certifications: Specialty credentials and professional memberships

- Years of experience: Time in practice and specific procedure expertise

- Technology investments: Modern equipment and treatment techniques

- Patient reviews: Online testimonials and reputation in the community

- Treatment philosophy: Preventive focus versus intervention-heavy approaches

Choosing a dental clinic that accepts insurance provides convenience and cost savings, but shouldn't compromise quality expectations. The best dental practices combine network participation with clinical excellence, modern technology, and patient-centered care.

Texas patients benefit from researching multiple providers before committing to treatment. Visit offices, meet dentists, and ask detailed questions about their approach to care, sterilization protocols, and emergency availability.

Geographic Accessibility and Convenience

Location matters significantly when selecting dental care providers. Network restrictions sometimes limit choices in certain geographic areas, particularly in rural or underserved regions of Texas.

Urban vs Rural Network Availability

Metropolitan areas like Austin, San Antonio, and Houston typically offer extensive in-network options. Patients in these markets can find multiple participating dentists within short driving distances. Dental Plus Clinic maintains locations across Texas to serve patients in diverse communities.

Rural areas present different challenges:

- Fewer total dental practices available

- Limited network participation among local providers

- Longer travel distances to reach in-network dentists

- Potential gaps in specialty services requiring referrals

Travel costs and time investments must factor into network decision-making. Driving 45 minutes each way to save $50 on a cleaning may not represent practical value when accounting for fuel, time off work, and convenience.

Families juggling busy schedules often prioritize proximity over marginal cost savings. A nearby out-of-network dentist offering evening and weekend appointments might deliver better overall value than a distant in-network provider with limited availability.

Plan Types and Network Flexibility

Different dental insurance structures impose varying levels of network restrictions. Understanding your specific plan design clarifies how much flexibility you have when choosing providers.

PPO Plans

Preferred Provider Organization (PPO) plans offer the most flexibility. These plans allow you to visit any licensed dentist but provide financial incentives for choosing network providers. You'll pay less out-of-pocket with in-network dentists but retain the option to go out-of-network for specialized care or personal preferences.

The differences between PPO and DHMO dental plans significantly impact your provider choices and cost structures.

DHMO Plans

Dental Health Maintenance Organization (DHMO) plans require you to select a primary care dentist from the network. These plans typically offer no coverage for out-of-network care except in emergencies. DHMO plans feature lower premiums but restrict provider choices more severely.

Indemnity Plans

Traditional indemnity plans allow complete provider freedom. You can visit any dentist, and insurance reimburses a percentage of usual and customary charges. These plans rarely distinguish between in-network and out-of-network providers but often carry higher premiums and deductibles.

| Plan Type | Network Requirement | Out-of-Network Coverage | Monthly Premium |

|---|---|---|---|

| PPO | Preferred, Not Required | Partial Coverage | Moderate |

| DHMO | Required | Emergency Only | Low |

| Indemnity | None | Full Coverage | High |

Claim Filing and Administrative Burden

The administrative experience differs substantially between network options. In-network dentists handle most insurance paperwork, while out-of-network care often requires patient involvement in claim submission and follow-up.

In-Network Administrative Process

Network dentists typically:

- Verify insurance coverage before appointments

- Submit claims directly to carriers electronically

- Accept assignment of benefits

- Wait for insurance payment before billing patients

- Handle claim disputes and resubmissions

This streamlined process minimizes patient involvement and reduces payment uncertainty. You receive treatment, pay your estimated portion, and the office handles the insurance relationship.

Out-of-Network Claim Procedures

Out-of-network care may require you to:

- Pay the full fee at the time of service

- Request itemized receipts and procedure codes

- Complete and submit claim forms yourself

- Wait for reimbursement checks from insurance

- Follow up on delayed or denied claims

- Appeal underpayments or coverage disputes

The administrative burden of out-of-network care shouldn't be underestimated. Managing claim submissions, tracking reimbursements, and resolving payment issues demands time and attention many patients prefer to avoid.

Some out-of-network dentists offer courtesy billing, submitting claims on your behalf despite lacking network contracts. This service reduces administrative hassles while maintaining the dentist's fee autonomy.

Emergency Care and Network Restrictions

Dental emergencies don't respect network boundaries. Understanding how your plan handles urgent care outside normal business hours or geographic areas helps you prepare for unexpected situations.

Most dental insurance plans recognize emergency care differently than routine services. When you experience severe pain, trauma, or infection requiring immediate attention, network restrictions often relax or disappear entirely.

Emergency Coverage Provisions

Typical emergency exceptions include:

- Geographic limitations: Coverage extends to out-of-network providers when traveling

- After-hours care: Network requirements waive for urgent weekend or evening needs

- Specialist referrals: Coverage applies when network lacks necessary specialists

- Immediate stabilization: Initial emergency treatment receives full benefits regardless of provider

Check your specific plan documents for emergency provisions. Some plans require you to visit network providers for follow-up care after initial emergency stabilization, even if the emergency dentist was out-of-network.

Dental emergency services require prompt attention. Don't delay treatment due to network concerns when facing serious dental problems.

Specialist Referrals and Advanced Treatments

Complex dental procedures often require specialists like periodontists, endodontists, or oral surgeons. Network status becomes more complicated when coordinating care between general dentists and specialists.

Specialty Network Considerations

Insurance plans typically maintain separate networks for specialists. Your general dentist might be in-network while the referred specialist operates out-of-network, or vice versa. This creates scenarios where:

- Referrals cross network boundaries

- Coordination of benefits becomes complex

- Prior authorization requirements vary

- Coverage percentages shift unexpectedly

Advanced procedures like dental implants, orthodontics, and full mouth reconstructions involve higher costs where network status dramatically impacts patient expenses. A $3,000 implant might cost you $1,500 in-network but $2,100 out-of-network after insurance reimbursement.

Dental implant procedures represent significant investments. Patients should verify specialist network status and obtain pre-authorization before beginning treatment to avoid unexpected costs.

Some specialists don't participate in any insurance networks, particularly those offering premium services or advanced techniques. When seeking cutting-edge treatments, patients may need to accept out-of-network costs regardless of preferences.

Long-Term Relationship Building

Continuity of care delivers measurable benefits in dentistry. Establishing long-term relationships with dental providers enables them to:

- Track oral health changes over years

- Recognize developing problems early

- Maintain comprehensive treatment records

- Understand patient preferences and anxieties

- Coordinate multi-phase treatment plans effectively

Network changes disrupt these relationships. Insurance companies periodically renegotiate contracts, adding or removing providers from networks. A dentist who's in-network today might drop out next year, forcing you to choose between maintaining the relationship or staying in-network.

Network Stability Factors

Consider network stability when selecting providers:

- Large network participation: Dentists in multiple networks face less disruption risk

- Established practices: Long-standing businesses demonstrate commitment to community

- Contract history: Ask how long they've participated in your specific network

- Future plans: Inquire about their network participation intentions

- Alternative arrangements: Discuss options if network status changes

Building relationships with practices like Dental Plus Clinic that maintain broad network participation provides stability against insurance industry volatility.

Making the Network Decision

Choosing between in-network vs out-of-network dentists requires weighing multiple factors against your personal circumstances, financial situation, and dental health needs.

Decision Framework

Evaluate these key questions:

Financial capacity: Can you absorb higher out-of-pocket costs for preferred providers?

Dental health status: Do you need extensive work where network savings compound significantly?

Geographic constraints: Are quality in-network options conveniently accessible?

Provider relationships: Do you have an established dentist you're reluctant to leave?

Insurance stability: How frequently does your employer change dental plans?

Treatment philosophy: Do you value clinical autonomy over cost optimization?

| Priority Level | Choose In-Network | Choose Out-of-Network |

|---|---|---|

| Maximum savings | Best choice | Not recommended |

| Specific dentist preference | Only if available | Acceptable |

| Extensive treatment needs | Highly recommended | Expensive |

| Limited network options | May require | Good alternative |

| Clinical autonomy desired | Adequate | Preferred |

The process of finding a dentist that accepts insurance in Texas starts with verifying network participation through your insurance carrier's online directory or customer service line.

Verifying Network Status

Insurance network directories become outdated quickly. Providers join and leave networks regularly, making verification essential before scheduling appointments.

Verification Best Practices

Confirm network status through multiple channels:

- Call the dental office directly: Ask if they participate in your specific plan

- Contact insurance customer service: Request current provider confirmation

- Check online directories: Use carrier websites for preliminary research

- Request written confirmation: Ask for documentation of network participation

- Verify coverage details: Confirm which services qualify for in-network rates

Don't assume network status based on past participation or general acceptance of your insurance carrier. A dentist might accept some plans from an insurer while remaining out-of-network for others.

Some insurance companies operate multiple networks with different provider lists. Confirm your dentist participates in your exact plan network, not just a general carrier network.

When researching Texas providers, consider visiting Dental Plus Clinic locations in New Braunfels, Seguin, or Leander to discuss network participation and available services.

Annual Benefit Maximization Strategies

Strategic planning helps maximize dental insurance benefits regardless of network choice. Understanding how benefits reset, accumulate, and expire enables smarter timing of dental procedures.

Timing Major Treatments

Coordinate expensive procedures with benefit periods:

- Split treatments across calendar years: Divide major work to access two annual maximums

- Front-load preventive care: Use full benefits early for cleanings and exams

- Plan elective procedures strategically: Schedule cosmetic work when benefits remain unused

- Coordinate family treatments: Stagger procedures to optimize household benefit usage

Preventive care delivers maximum insurance value because most plans cover cleanings, exams, and x-rays at 100% with no deductible. These services preserve your annual maximum for unexpected restorative needs.

Regular dental exams and cleanings prevent costly problems while maximizing insurance benefits. In-network preventive visits typically cost patients nothing out-of-pocket.

Understanding Usual and Customary Rates

Insurance companies determine "usual and customary" (UCR) rates by surveying dental fees in specific geographic areas. These rates establish maximum reimbursement amounts for out-of-network care.

UCR Rate Impacts

When visiting out-of-network dentists:

- Insurance bases reimbursement on UCR, not actual charges

- You pay the difference between actual fees and UCR rates

- UCR rates vary by procedure, location, and insurance carrier

- Appeals processes exist for unreasonably low UCR determinations

A dentist charging $200 for a filling might trigger only $150 UCR reimbursement from insurance. If your plan covers 70% of out-of-network basic services, you'd receive $105 from insurance and owe the dentist $95 ($200 minus $105).

UCR calculations lack transparency and often favor insurance companies over patients. The billing differences between network options significantly affect your final costs.

Negotiating Fees and Payment Plans

Out-of-network dentists offer more flexibility for fee negotiations and payment arrangements since they're not bound by insurance contracts.

Payment Negotiation Strategies

Consider these approaches:

- Cash payment discounts: Offer upfront payment for reduced fees

- Treatment plan modifications: Discuss phased approaches spreading costs

- Payment plans: Negotiate interest-free monthly installments

- Competitive pricing: Reference in-network rates during discussions

- Bundled services: Request package pricing for multiple procedures

Many dental practices value payment certainty over maximum fees. Offering guaranteed payment might yield 10-20% discounts from standard rates.

Insurance filing as courtesy billing represents another negotiation point. Some out-of-network dentists submit claims on your behalf to reduce administrative burdens, potentially swaying your provider decision.

Children's Dental Care and Networks

Pediatric dental needs present unique network considerations. Children require consistent preventive care and often need orthodontic treatments spanning multiple years.

Pediatric Network Factors

Evaluate children's dental networks based on:

- Pediatric specialist availability: Age-appropriate care from trained providers

- Preventive program participation: Sealants, fluoride treatments, early intervention

- Orthodontic coverage: Braces and alignment treatments

- Behavioral management: Experience handling anxious or special needs children

- Family convenience: Ability to see multiple family members at one practice

Pediatric dentistry services establish lifelong oral health foundations. Choosing in-network pediatric dentists makes regular preventive visits affordable for growing families.

Children accumulate dental expenses over 18+ years. Small per-visit savings compound substantially across childhood when staying in-network consistently.

Insurance Denial Appeals

Claim denials happen with both network options but require different response strategies. Understanding how to appeal denied dental insurance claims protects your financial interests.

Common Denial Reasons

Insurance companies deny claims for:

- Pre-existing condition clauses: Treatment for problems before coverage began

- Missing documentation: Insufficient x-rays, narratives, or justification

- Alternative treatment arguments: Insurance suggests cheaper alternatives

- Frequency limitations: Procedures performed too soon after previous treatment

- Plan exclusions: Services not covered under your specific policy

In-network dentists handle most appeals because they maintain direct relationships with insurance carriers and understand specific plan requirements. Out-of-network appeals often fall to patients, requiring more effort and insurance policy knowledge.

Appeal success rates improve when you:

- Submit comprehensive clinical documentation

- Reference specific policy language supporting coverage

- Provide detailed treatment narratives from dentists

- Escalate through formal appeal channels

- Request peer-to-peer reviews between dentists

- Contact state insurance commissioners when appropriate

Multi-Location Practices and Network Benefits

Dental practices operating multiple locations often maintain consistent network participation across all offices. This provides patients flexibility to visit different locations while preserving in-network benefits.

Multi-Location Advantages

Practices with several offices offer:

- Geographic convenience: Choose locations based on work, home, or errands

- Scheduling flexibility: Access more appointment times across multiple calendars

- Consistent care standards: Unified protocols and quality assurance

- Shared records: Seamless access to treatment history at any location

- Specialist access: Centralized referral networks and coordination

Dental Plus Clinic operates locations throughout Texas, including Beeville and Converse, providing patients convenient access to comprehensive dental services while maintaining network participation.

Future-Proofing Your Dental Care

Healthcare landscapes constantly evolve. Insurance networks change, dentists retire, practices relocate, and family circumstances shift. Making sustainable long-term decisions about dental care requires considering future scenarios.

Long-Term Planning Considerations

Think ahead about:

Career mobility: Will job changes affect insurance networks?

Family growth: How might children impact dental care needs?

Health trajectories: Do chronic conditions suggest increasing dental needs?

Geographic stability: Are relocations likely requiring new providers?

Retirement planning: How will Medicare and supplemental coverage work?

Establishing relationships with stable, multi-location practices provides continuity through life transitions. The understanding you build with consistent providers delivers value beyond immediate cost savings.

Selecting between in-network vs out-of-network dentists ultimately depends on balancing financial considerations, quality expectations, and personal circumstances unique to your situation. Texas families benefit from thoroughly researching provider credentials, verifying network participation, and understanding their specific insurance plan details before committing to dental relationships. Whether you prioritize maximum cost savings through in-network care or value clinical autonomy through out-of-network providers, Dental Plus Clinic combines network participation with comprehensive dental services, modern technology, and patient-focused care across five convenient Texas locations to serve your family's oral health needs.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}