Understanding dental implants insurance cover can feel overwhelming, especially when you’re facing the prospect of tooth replacement and want to make informed financial decisions. In Texas, where dental care costs vary across regions and insurance policies differ significantly, knowing what your plan covers before committing to implant treatment is essential. This comprehensive guide examines how insurance providers approach dental implant coverage, what components of the procedure might be covered, and practical strategies for managing costs at dental practices throughout the Lone Star State.

Understanding Dental Implants Insurance Cover Basics

Dental implants represent one of the most advanced tooth replacement solutions available in 2026, but they also rank among the most expensive dental procedures. Most traditional dental insurance plans categorize implants differently than routine procedures like cleanings or fillings.

The majority of dental insurance policies classify implants as elective or cosmetic procedures. This classification significantly impacts coverage, as insurers traditionally view implants as optional rather than medically necessary. However, the landscape is gradually changing as more insurance companies recognize the long-term health benefits of implants over alternatives like bridges or dentures.

Coverage Variations Across Insurance Plans

Insurance coverage for dental implants varies dramatically depending on several factors:

- Plan type: PPO plans typically offer more flexibility than HMO plans

- Premium level: Higher-premium plans often include better coverage for major procedures

- Employer-sponsored versus individual plans: Group plans frequently provide more comprehensive coverage

- Insurance provider: Some carriers are more progressive in covering implant procedures

According to Humana’s dental implant coverage guidelines, most standard dental insurance plans cover between 0% and 50% of implant costs when coverage is available. The specific percentage depends on how your policy classifies the procedure and whether medical necessity can be demonstrated.

What Components of Dental Implants Might Be Covered

Even when full dental implants insurance cover isn’t available, certain components of the implant procedure may receive partial coverage. Understanding which parts of the treatment might be covered helps you estimate your out-of-pocket expenses more accurately.

The Implant Post and Surgical Placement

The titanium or zirconia post that serves as the artificial tooth root is the most expensive component. Unfortunately, this portion receives coverage least frequently. Most insurance companies exclude the surgical placement of the implant post itself, viewing it as the cosmetic or elective portion of treatment.

However, some progressive insurance plans now offer partial coverage when the implant is deemed medically necessary. This determination typically requires documentation showing that alternatives like bridges would compromise adjacent healthy teeth or that bone loss necessitates implant placement for structural reasons.

Abutment and Crown Coverage

Many insurance plans that exclude the implant post itself may still cover the abutment and crown. Aspen Dental’s insurance information explains that the crown portion is sometimes covered at the same rate as a crown placed on a natural tooth.

This partial coverage approach means you might receive 50% coverage on the crown component, which typically costs $1,000-$3,000, even if the $1,500-$2,500 implant post isn’t covered. At Dental Plus Clinic’s Texas locations, treatment coordinators help patients identify which components their insurance covers before beginning treatment.

| Implant Component | Typical Cost Range | Likely Coverage Level | Common Classification |

|---|---|---|---|

| Diagnostic Imaging | $200-$500 | 50%-80% | Diagnostic/Preventive |

| Implant Post | $1,500-$2,500 | 0%-30% | Major/Cosmetic |

| Abutment | $300-$700 | 0%-50% | Major Restorative |

| Crown | $1,000-$3,000 | 30%-50% | Major Restorative |

| Bone Grafting | $500-$2,500 | 0%-50% | Major/Surgical |

Diagnostic and Preparatory Procedures

Preliminary procedures often receive better coverage than the implant itself. Diagnostic imaging like X-rays and CT scans may be covered at 80% or higher under diagnostic benefits. These imaging procedures are essential for proper dental implant procedure planning and usually cost between $200-$500.

Tooth extraction prior to implant placement typically receives coverage similar to other surgical extractions, often at 50%-80%. If bone grafting is required to ensure sufficient bone density for implant stability, coverage depends on whether the procedure is documented as medically necessary versus purely cosmetic preparation.

Medical Necessity and Insurance Approval

The concept of medical necessity plays a crucial role in dental implants insurance cover. Insurance companies are more likely to approve claims when implants address functional problems rather than purely aesthetic concerns.

Documenting Medical Necessity

Several scenarios strengthen the case for medical necessity:

- Traumatic injury: Tooth loss from accidents rather than decay or natural causes

- Congenital conditions: Missing teeth due to developmental disorders

- Severe bone loss: Cases where dentures cannot be retained without implant support

- Adjacent tooth preservation: Situations where bridges would require reducing healthy teeth

Your dental provider must document these conditions thoroughly. At practices like Dental Plus Clinic, comprehensive documentation includes detailed clinical notes, diagnostic imaging, and written justification explaining why alternative treatments are inadequate.

The Pre-Authorization Process

Submitting a pre-authorization request before beginning treatment provides clarity on what your insurance will cover. This process involves:

- Submitting diagnostic records and treatment plans to your insurance company

- Providing clinical justification for the proposed treatment

- Waiting 2-4 weeks for the insurance company’s determination

- Receiving a breakdown of covered services and patient responsibility

Research on dental implant insurance coverage indicates that pre-authorization significantly reduces surprise bills and claim denials. Even when coverage is limited, knowing your financial responsibility upfront allows better treatment planning and budgeting.

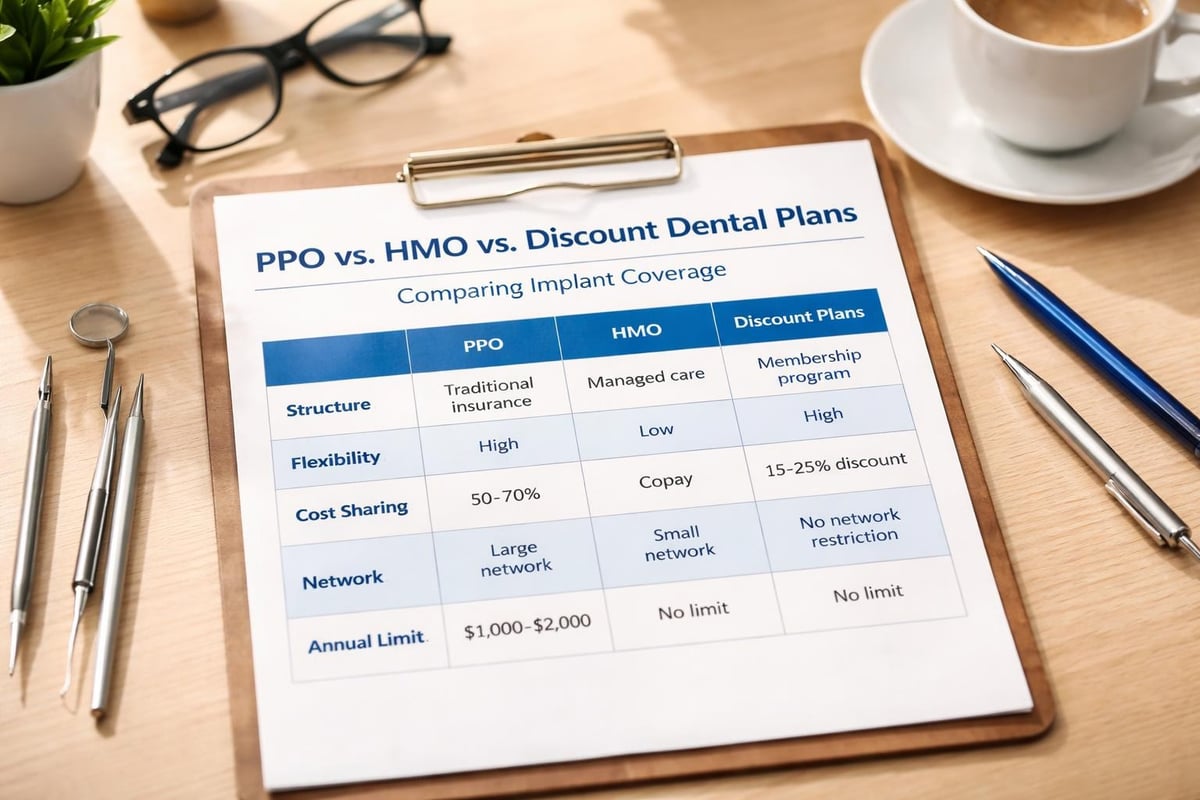

Insurance Plan Types and Implant Coverage

Different insurance structures approach dental implants insurance cover with varying philosophies. Understanding your plan type helps set realistic expectations.

PPO Plans and Flexibility

Preferred Provider Organization (PPO) plans typically offer the most flexibility for implant coverage. These plans usually allow you to visit any dentist, though staying in-network reduces costs. PPO plans that cover implants generally do so at 50% after your deductible is met, subject to annual maximums.

The annual maximum limitation presents a significant challenge. Most dental PPO plans cap coverage at $1,500-$2,500 per year, which may not fully cover a single implant. Patients often spread treatment across multiple benefit years to maximize coverage.

HMO and DHMO Plans

Health Maintenance Organization (HMO) dental plans rarely cover implants. These plans focus on preventive and basic care with limited networks of providers. When implants are covered under DHMO plans, patients typically pay a discounted fee rather than receiving percentage-based coverage.

The restricted provider networks mean you must choose from approved dentists, which may limit access to experienced implant specialists. However, the trade-off is lower monthly premiums compared to PPO plans.

Discount Dental Plans

Discount dental plans aren’t insurance but membership programs offering reduced fees. These plans negotiate discounted rates with participating dentists, sometimes reducing implant costs by 20%-40%. While not providing traditional dental implants insurance cover, discount plans offer predictable savings without annual maximums or waiting periods.

Waiting Periods and Coverage Limitations

Even when your insurance plan includes implant coverage, several restrictions may apply that affect when and how you can access benefits.

Standard Waiting Periods

Most dental insurance plans impose waiting periods for major procedures:

- Preventive care: Immediate coverage

- Basic procedures: 3-6 month waiting period

- Major procedures (including implants): 6-12 month waiting period

These waiting periods mean you cannot purchase insurance after discovering you need an implant and expect immediate coverage. Planning ahead is essential when considering implant treatment.

Annual Maximum Limits

The annual maximum represents the total amount your insurance pays for all dental care in a calendar year. Understanding insurance plans and their limits reveals that standard maximums of $1,500-$2,500 often fall short of covering complete implant treatment costing $3,000-$6,000 per tooth.

Some strategies for working within annual maximums include:

- Splitting treatment across two benefit years

- Combining insurance coverage with financing for the balance

- Prioritizing which teeth to replace based on functional importance

- Exploring supplemental dental insurance for additional coverage

Lifetime Maximums on Implants

Certain insurance plans impose lifetime maximums specifically for implants, separate from annual limits. A plan might cover implants at 50% but cap total lifetime implant benefits at $2,000-$3,000. This limitation means even with coverage, you might exhaust benefits after one or two implants.

Alternative Coverage Sources Beyond Traditional Dental Insurance

When traditional dental implants insurance cover proves insufficient, alternative coverage sources may help bridge the financial gap.

Medical Insurance for Dental Implants

In specific circumstances, medical insurance may cover dental implants. According to oral surgery specialists, medical policies sometimes cover implants when tooth loss results from:

- Accidental injury or trauma

- Cancer treatment requiring tooth extraction

- Congenital disorders affecting tooth development

- Medical conditions necessitating tooth removal

Medical insurance coverage typically requires extensive documentation proving the dental work addresses a medical condition rather than a purely dental issue. Coordination between your dentist, oral surgeon, and medical insurance provider is essential for successful claims.

Medicare and Medicaid Considerations

Traditional Medicare does not cover dental implants, as routine dental care falls outside Medicare’s scope. However, Medicare Advantage plans (Part C) offered by private insurers may include dental benefits covering a portion of implant costs.

Medicaid coverage varies by state. In Texas, adult Medicaid dental benefits are limited, typically covering only emergency extractions and pain relief. Detailed information on Medicaid and implant coverage confirms that implants are rarely covered under standard Medicaid programs unless exceptional circumstances exist.

Health Savings Accounts and Flexible Spending Accounts

HSAs and FSAs offer tax-advantaged ways to pay for dental implants insurance cover gaps. Both account types allow you to use pre-tax dollars for qualified medical and dental expenses, including implants. For 2026, HSA contribution limits reach $4,150 for individuals and $8,300 for families.

The tax savings effectively reduce your implant costs by your marginal tax rate. If you’re in the 22% tax bracket, using $5,000 from your HSA for implants saves $1,100 in taxes compared to paying with after-tax dollars.

Strategies for Maximizing Insurance Benefits

Even with limited dental implants insurance cover, strategic planning helps maximize the benefits available under your policy.

Timing Treatment Strategically

Coordinating treatment with your insurance benefit year maximizes coverage. Consider these approaches:

- Year-end and year-beginning split: Schedule extraction and bone grafting in December, then place the implant in January to access two years of benefits

- Spread multiple implants: If you need several implants, complete one per benefit year to fully utilize annual maximums

- Combine with other procedures: Schedule implants alongside covered procedures to make full use of your annual maximum

Verifying Coverage Before Treatment

Consulting with insurance providers and dental offices before beginning treatment prevents financial surprises. Effective verification includes:

- Requesting a detailed breakdown of covered procedures

- Confirming your remaining annual maximum

- Checking whether waiting periods apply

- Understanding deductible requirements

- Verifying in-network status of your dental provider

The team at locations like Dental Plus Clinic in Seguin, Converse, New Braunfels, Leander, and Beeville routinely handles insurance verification, helping patients understand their coverage before treatment begins.

Appealing Denied Claims

If your insurance denies coverage, appealing the decision sometimes succeeds, particularly when medical necessity is documented. Effective appeals include:

- Additional clinical documentation supporting medical necessity

- Letters from your dentist explaining why alternatives are inadequate

- Supporting research on long-term health outcomes of implants versus alternatives

- Detailed cost comparisons showing implants prevent future problems

Appeals processes typically involve 2-3 levels of review, and persistence sometimes results in approved coverage even after initial denials.

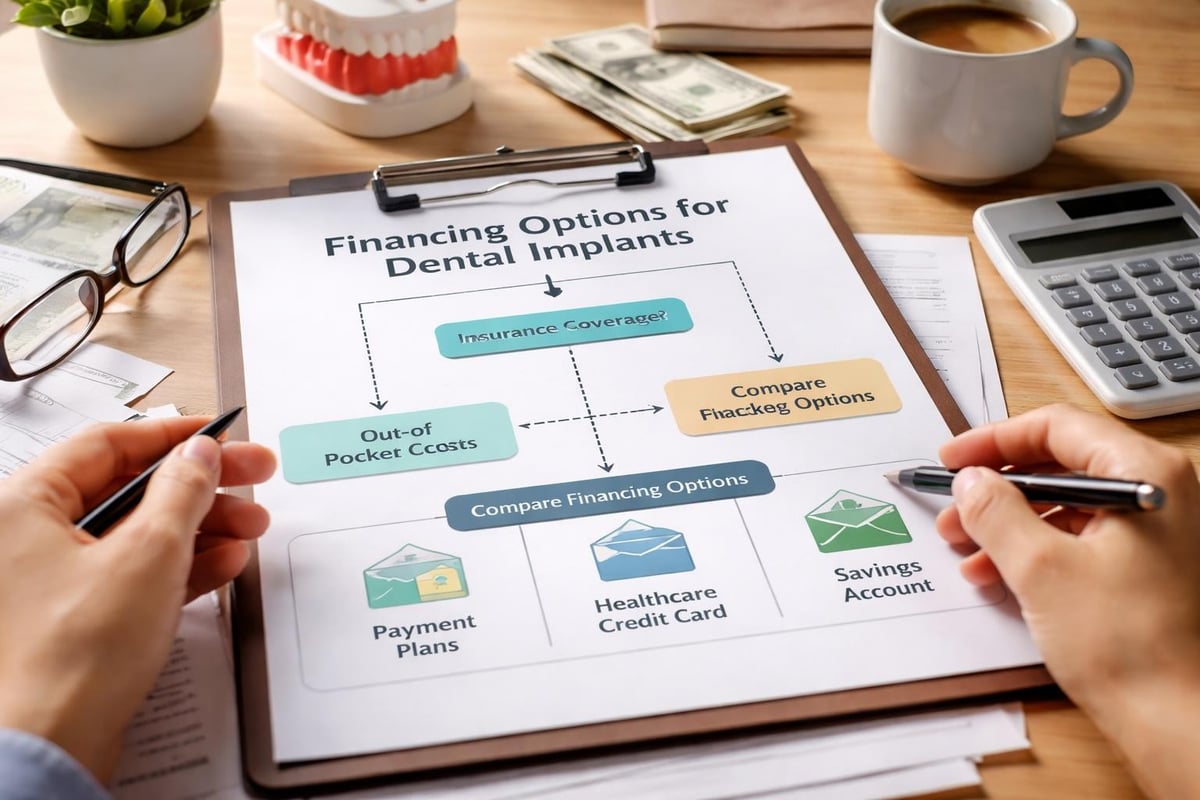

Financing Options When Insurance Coverage Falls Short

Most patients need to supplement dental implants insurance cover with other payment methods to afford complete treatment.

In-House Financing Plans

Many dental practices, including Dental Plus Clinic’s Texas offices, offer in-house payment plans. These arrangements typically feature:

- Zero or low-interest financing for qualified patients

- Flexible payment terms from 6-24 months

- No credit check options for smaller balances

- Automatic payment plans for convenience

In-house financing often proves more accessible than third-party lenders and helps patients begin treatment without waiting to save the full amount.

Third-Party Healthcare Financing

Companies specializing in healthcare financing provide loans specifically for medical and dental procedures. Popular options include CareCredit, LendingClub Patient Solutions, and Alphaeon Credit. These programs offer:

- Promotional interest-free periods (often 6-24 months)

- Extended payment terms for larger procedures

- Instant approval processes

- Coverage for family members under one account

The key to benefiting from promotional financing is paying off the balance before the promotional period ends, as deferred interest often applies retroactively to the original balance.

Dental Savings Plans

Beyond traditional dental implants insurance cover, membership-based savings plans provide predictable discounts. Precision Dental explains how these plans work differently than insurance, offering percentage discounts on all procedures without annual maximums or waiting periods.

Membership fees typically range from $100-$300 annually for individuals or $200-$500 for families, with implant discounts of 20%-40% at participating providers.

Cost Comparison: Insurance Coverage Versus Out-of-Pocket

Understanding real-world cost scenarios helps patients make informed decisions about dental implant treatment with varying levels of insurance coverage.

Scenario 1: No Insurance Coverage

Without any dental implants insurance cover, patients pay the full cost of treatment. For a single implant including post, abutment, and crown, costs in Texas typically range from $3,000-$6,000 depending on location and complexity.

At Dental Plus Clinic locations throughout Texas, transparent pricing helps patients understand total costs upfront. Additional procedures like bone grafting ($500-$2,500) or sinus lifts ($1,500-$3,000) increase total investment when required.

Scenario 2: Partial Coverage for Crown Only

Many patients experience this common coverage scenario. If insurance covers the crown at 50% with a $1,500 cost, the patient receives $750 in benefits. The remaining $4,500-$5,250 for the implant post, abutment, and uncovered crown portion becomes the patient’s responsibility.

This partial coverage reduces overall costs by approximately 15%-20%, making treatment more accessible while still requiring substantial out-of-pocket investment.

Scenario 3: Comprehensive Coverage with Limitations

The most favorable insurance scenario involves coverage for multiple implant components subject to annual maximums. If a plan covers diagnostic imaging at 80%, surgical procedures at 50%, and restorative work at 50%, potential insurance payments might reach $2,000-$2,500.

However, annual maximums cap total benefits. Even with comprehensive percentage coverage, the $1,500-$2,500 maximum means patients still pay $2,500-$4,000 per implant.

| Coverage Scenario | Total Implant Cost | Insurance Pays | Patient Pays | Effective Discount |

|---|---|---|---|---|

| No Coverage | $5,000 | $0 | $5,000 | 0% |

| Crown Only (50%) | $5,000 | $750 | $4,250 | 15% |

| Partial Multi-Component | $5,000 | $1,500 | $3,500 | 30% |

| Maximum Coverage Limited | $5,000 | $2,000 | $3,000 | 40% |

Questions to Ask Your Insurance Provider

Before proceeding with dental implant treatment, asking specific questions helps clarify your dental implants insurance cover and prevents misunderstandings.

Coverage-Specific Questions

Direct questions about coverage include:

- Does my plan cover any portion of dental implant treatment?

- What specific components (post, abutment, crown) are covered?

- What percentage does my plan cover for covered components?

- Is pre-authorization required for implant procedures?

- How is medical necessity determined for implant coverage?

Financial Limitation Questions

Understanding financial constraints is equally important:

- What is my annual maximum benefit for this year?

- How much of my annual maximum have I already used?

- Does my plan have a lifetime maximum for implants specifically?

- What is my deductible, and has it been met this year?

- Are there waiting periods that apply to implant coverage?

Provider Network Questions

Network status affects both coverage levels and out-of-pocket costs:

- Is my chosen dental provider in-network for my plan?

- How does coverage differ for in-network versus out-of-network providers?

- Can I obtain out-of-network benefits if my preferred dentist isn’t contracted?

- What documentation is needed for out-of-network reimbursement?

How Coverage Has Evolved in Recent Years

The dental insurance industry’s approach to dental implants insurance cover has shifted significantly over the past decade as implants have become more common and their long-term benefits more documented.

Historical Perspective on Implant Coverage

Before 2015, fewer than 10% of dental insurance plans offered any coverage for implants. Articles examining insurance evolution note that insurers historically classified all implants as cosmetic, making coverage nearly impossible to obtain.

The classification reflected outdated perspectives that viewed dental implants as luxury items rather than medically beneficial treatments. As research demonstrated implants’ advantages in preventing bone loss, maintaining facial structure, and improving quality of life, insurance companies gradually reconsidered their positions.

Current Coverage Trends

By 2026, approximately 30%-40% of dental insurance plans include some level of implant coverage, though extent varies widely. Aflac’s coverage information highlights this trend, noting more insurers recognize implants as valid treatment options.

Progressive insurance companies now offer:

- Implant coverage in premium plan tiers

- Higher annual maximums to accommodate implant costs

- Reduced waiting periods for implant procedures

- Coverage for implant maintenance and repairs

Future Coverage Predictions

Industry experts predict continued expansion of dental implants insurance cover as implants become standard care. Factors driving this trend include:

- Growing clinical evidence supporting implant longevity and outcomes

- Aging population requiring more tooth replacement solutions

- Cost reductions as implant technology becomes more efficient

- Consumer demand for comprehensive dental coverage

Some insurance analysts predict that by 2030, implants will receive coverage similar to current bridges and dentures, with 50%-60% of plans offering substantive benefits.

Regional Considerations for Texas Residents

Geographic location within Texas can influence both dental implants insurance cover availability and treatment costs.

Insurance Availability Across Texas

Major insurance carriers operate throughout Texas, but plan offerings vary by region. Urban areas like Houston, Dallas, San Antonio, and Austin typically have more insurance options and competitive pricing than rural regions.

Employer-sponsored insurance in Texas varies by industry. Energy sector employees often receive more comprehensive dental benefits than retail or hospitality workers, affecting access to implant coverage.

Cost Variations by Location

Treatment costs fluctuate based on local economic conditions and practice overhead. Metropolitan areas generally charge more than smaller cities, though competition may drive some urban prices down.

Patients seeking treatment at Dental Plus Clinic’s multiple Texas locations find consistent pricing across Beeville, Seguin, New Braunfels, Leander, and Converse, providing cost predictability regardless of which office they visit.

Texas-Specific Insurance Regulations

Texas insurance regulations affect dental implants insurance cover in several ways. The state requires certain minimum coverages for dental plans but does not mandate implant coverage. Texas law does require transparency in coverage explanations, helping patients understand their benefits.

Texas residents can access state resources for insurance disputes, including the Texas Department of Insurance, which mediates disagreements between patients and insurers over coverage denials.

Making Informed Decisions About Implant Treatment

Understanding dental implants insurance cover represents just one component of making informed treatment decisions. Balancing financial considerations with health needs requires comprehensive evaluation.

Comparing Implants to Alternatives

When insurance coverage is limited, some patients consider alternatives. Traditional bridges often receive better coverage than implants, typically at 50% after deductibles. However, bridges require modifying adjacent teeth and last 7-15 years compared to implants’ 20+ year lifespan.

Dentures also receive more consistent insurance coverage, usually at 50%-80%. Yet dentures require regular replacement, don’t prevent bone loss, and may compromise quality of life. Comparing treatment options helps patients weigh immediate costs against long-term value.

Long-Term Financial Analysis

While implants require higher upfront investment, long-term cost analysis often favors them over alternatives:

- Implants: $5,000 initial cost, minimal maintenance, 25+ year lifespan = $200 per year

- Bridge: $2,500 initial cost, $2,500 replacement every 10 years = $250 per year

- Dentures: $1,500 initial cost, $1,500 replacement every 5-7 years, relining costs = $300+ per year

This analysis doesn’t account for implants’ additional benefits like bone preservation and improved function, which provide value beyond direct cost comparisons.

Quality of Life Considerations

Financial factors matter, but health and quality of life considerations are equally important. Implants offer advantages that transcend insurance coverage:

- Functionality: Chewing efficiency matches natural teeth

- Bone preservation: Prevents jawbone deterioration from tooth loss

- Aesthetic results: Natural appearance and feel

- Confidence: No concerns about slipping dentures or visible gaps

- Longevity: Potential lifetime solution with proper care

Patients focused solely on maximizing dental implants insurance cover might choose suboptimal treatments. Balancing insurance benefits with long-term health outcomes produces better decisions.

Working With Your Dental Provider on Insurance

Successful navigation of dental implants insurance cover requires collaboration between patients, dental providers, and insurance companies. Dental practices with experienced administrative staff provide invaluable assistance in this process.

What Your Dental Office Can Do

Quality dental practices offer comprehensive insurance support:

- Verify coverage before treatment begins

- Submit pre-authorization requests with detailed documentation

- Provide itemized treatment plans showing covered versus non-covered portions

- File insurance claims on your behalf

- Follow up on delayed or denied claims

- Appeal denials with additional clinical justification

What Patients Should Provide

Patients contribute to successful insurance processing by:

- Providing accurate, current insurance information

- Understanding their policy details and limitations

- Responding promptly to requests for additional information

- Maintaining realistic expectations about coverage

- Communicating openly about budget constraints

Creating Treatment Plans That Maximize Benefits

Experienced dental providers structure treatment plans to optimize insurance benefits. This might involve sequencing procedures across benefit years, documenting medical necessity thoroughly, or suggesting alternative approaches that achieve similar results with better coverage.

At Dental Plus Clinic, treatment coordinators work with patients to develop financial plans that combine insurance benefits, payment plans, and alternative financing to make implant treatment accessible.

Understanding the Claims and Reimbursement Process

Even with dental implants insurance cover, understanding how claims work prevents confusion and delays in receiving benefits.

How Dental Claims Are Processed

The typical dental claim process follows these steps:

- Treatment completion: Your dentist performs the procedure

- Claim submission: The dental office submits detailed claim forms to your insurer

- Claim review: Insurance company evaluates the claim against policy terms

- Explanation of benefits: Insurer sends EOB showing what’s covered and what you owe

- Payment processing: Insurance pays the dental office or reimburses you directly

- Patient balance: You pay any remaining balance to the dental office

This process typically takes 2-6 weeks, though complex claims may require longer review periods.

Common Claim Denial Reasons

Understanding why claims get denied helps avoid problems:

- Procedure not covered: Implants excluded from policy

- Missing documentation: Insufficient clinical justification

- Exceeded maximums: Annual or lifetime limits reached

- Waiting period not met: Treatment received before eligibility began

- Pre-authorization required: Procedure performed without required approval

- Out-of-network provider: Benefits reduced or unavailable for non-contracted dentists

Addressing Denied Claims

When claims are denied, several options exist:

- Request detailed explanation of denial reasons

- Submit additional documentation supporting medical necessity

- File formal appeal with insurance company

- Escalate to state insurance department if appeal fails

- Negotiate payment arrangements with dental provider for uncovered amounts

Persistence often pays off, particularly when denial reasons are technical rather than policy-based.

Special Considerations for Multiple Implants

Patients needing several implants face unique challenges regarding dental implants insurance cover, as costs multiply while annual maximums remain constant.

Full-Arch Restoration Coverage

Treatments like All-on-4 or All-on-6 implants that replace entire arches cost $15,000-$30,000 per arch. Standard insurance maximums of $1,500-$2,500 cover only a small fraction of these costs, typically 5%-15%.

Some patients explore these strategies for full-arch restoration:

- Spreading treatment across multiple years to access several years of benefits

- Combining dental and medical insurance when trauma or medical conditions are involved

- Negotiating package pricing with dental providers for cash payment

- Using healthcare financing for the substantial uncovered portion

Advanced implant options require careful financial planning given limited insurance coverage for extensive treatments.

Prioritizing Treatment When Resources Are Limited

When insurance benefits and personal resources cannot cover all needed implants, prioritization becomes necessary. Dentists typically recommend replacing teeth based on:

- Functional importance: Molars for chewing efficiency

- Bone preservation needs: Areas experiencing rapid bone loss

- Adjacent tooth protection: Preventing shifting and additional problems

- Aesthetic concerns: Visible teeth affecting confidence and social interaction

Strategic phasing of treatment allows patients to address the most critical needs first while planning for additional implants as finances permit.

Insurance Trends and What to Expect

As dental technology advances and implants become increasingly standard, dental implants insurance cover continues evolving.

Expanding Coverage Options

More insurance carriers now offer implant coverage as optional riders or in premium plan tiers. This trend allows consumers to choose higher-premium plans when they anticipate needing implants, similar to how medical insurance offers different coverage levels.

Some employers now offer multiple dental plan options, with basic plans excluding implants while premium options provide 50% coverage. This flexibility helps patients select coverage matching their anticipated needs.

Impact of Dental Technology Advances

Innovations in dental implant technology may influence future coverage. As techniques become more standardized and efficient, costs should decrease, potentially making coverage more feasible for insurers.

Computer-guided implant placement, same-day implants, and improved materials all contribute to better outcomes and efficiency. Insurance companies often expand coverage as procedures become more predictable and cost-effective.

Consumer Advocacy and Coverage Improvements

Patient advocacy groups increasingly pressure insurance companies to recognize implants as standard care rather than cosmetic procedures. This advocacy, combined with mounting clinical evidence of implants’ superiority to alternatives, gradually shifts industry perspectives.

Professional organizations like the American Dental Association continue educating insurers about implants’ health benefits, contributing to expanded coverage availability.

Final Thoughts

Understanding dental implants insurance cover empowers you to make informed decisions about your oral health while managing costs effectively. While coverage remains limited in many cases, strategic planning, thorough documentation, and exploring multiple payment options make implant treatment accessible to more patients. At Dental Plus Clinic, our experienced team helps patients navigate insurance complexities, maximize available benefits, and develop personalized payment plans that make quality implant treatment affordable across all our Texas locations.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}